-

@ bf47c19e:c3d2573b

2025-05-24 17:11:28

@ bf47c19e:c3d2573b

2025-05-24 17:11:28Originalni tekst na bitcoin-balkan.com.

Pregled sadržaja

- Odakle Potiče Bitcoin?

- Koje Probleme Rešava Bitcoin?

- Kako se Bitcoin razvijao u poslednjoj deceniji?

Bitcoin je peer to peer elektronski keš, novi oblik digitalnog novca koji se može prenositi između ljudi ili računara, bez potrebe za učestvovanjem pouzdanog posrednika (kao što je banka) i čije izdavanje nije pod kontrolom nijedne stranke.

Zamislite papirni dolar ili metalni novčić. Kad taj novac date drugoj osobi, ona ne mora da zna ko ste vi.

On samo treba da veruju da novac koji dobiju od vas nije falsifikat. Obično, proveravanje falsifikata „fizičkog“ novca, ljudi rade koristeći samo oči i prste ili koristeći specijalnu opremu za testiranje ukoliko se radi o značajnijoj sumi novca.

Većina plaćanja u našem digitalnom društvu vrši se putem Interneta korišćenjem neke posredničke usluge: kompanije za izdavanje kreditnih kartica poput Visa, snabdevača digitalnih plaćanja kao što je PayPal ili Apple Pay ili mrežne platforme poput WeChat u Kini.

Kretanje ka digitalnom plaćanju sa sobom donosi oslanjanje na nekog centralnog aktera koji mora odobriti i verifikovati svaku uplatu.

Priroda novca se promenila od fizičkog predmeta koji možete da nosite, prenesete i autentifikujete do digitalnih bitova koje mora da čuva i verifikuje treća strana koja kontroliše njihov prenos.

Odricanjem od gotovine u korist „udobnih“ digitalnih plaćanja, mi takođe stvaramo sistem u kome dajemo ogromna ovlašćenja onima koji bi poželeli da nas tlače.

Platforme za digitalno plaćanje postale su osnova distopijskih autoritarnih metoda kontrole, poput onih koje kineska vlada koristi za nadgledanje disidenata i sprečava građane, čije ponašanje im se ne svidja, da kupuju robu i plaćaju usluge.

Bitcoin nudi alternativu centralno kontrolisanom digitalnom novcu sa sistemom koji nam vraća prirodu korišćenja keša – čovek čoveku, ali u digitalnom obliku.

Bitcoin je digitalno sredstvo koje se izdaje i prenosi preko mreže međusobno povezanih računara, od koji svaki od njih samostalno potvrđuje da svi ostali igraju po pravilima.

Bitcoin Mreža

Odakle Potiče Bitcoin?

Bitcoin je izumela osoba ili grupa poznata pod pseudonimom Satoshi Nakamoto, oko 2008. godine.

Niko ne zna Satoshijev identitet, a koliko znamo, oni su nestali i o njima se godinama ništa nije čulo.

11.februara 2009. godine, Satoshi je pisao o ranoj verziji Bitcoin-a na mrežnom forumu za cypherpunkere, ljude koji rade na tehnologiji kriptografije i koji su zabrinuti za privatnost i slobodu pojedinca.

Iako ovo nije prvo zvanično objavljivanje Bitcoin-a, sadrži dobar rezime Satoshi-jevih motiva.

Razvio sam novi P2P sistem e-keša otvorenog koda pod nazivom Bitcoin. Potpuno je decentralizovan, bez centralnog servera ili pouzdanih stranki, jer se sve zasniva na kripto dokazima umesto na poverenju. […]

Osnovni problem konvencionalne valute je potpuno poverenje koje je potrebno za njeno funkcionisanje. Centralnoj banci se mora verovati da neće devalvirati valutu, ali istorija tradicionalnih valuta je puna primera kršenja tog poverenja. Bankama se mora verovati da drže naš novac i prenose ga elektronskim putem, ali one ga daju u talasima kreditnih balona sa delićem rezerve. Moramo im verovati sa našom privatnošću, verovati im da neće dozvoliti da kradljivci identiteta pokradu naše račune. Njihovi ogromni režijski troškovi onemogućavaju mikro plaćanja.

Generaciju ranije, višekorisnički time-sharing računarski sistemi imali su sličan problem. Pre pojave jake enkripcije, korisnici su morali da imaju pouzdanje u zaštitu lozinkom kako bi zaštitili svoje fajlove […]

Tada je jaka enkripcija postala dostupna širokim masama i više nije bilo potrebno poverenje. Podaci bi se mogli osigurati na način koji je fizički bio nemoguć za pristup drugima, bez obzira iz kog razloga, bez obzira koliko je dobar izgovor, bez obzira na sve.

Vreme je da imamo istu stvar za novac. Uz e-valutu zasnovanu na kriptografskom dokazu, bez potrebe da verujete posredniku treće strane, novac može biti siguran i transakcije mogu biti izvršene bez napora. […]

Rešenje Bitcoin-a je korišćenje peer-to-peer mreže za proveru dvostruke potrošnje. Ukratko, mreža radi poput distribuiranog servera vremenskih žigova, obeležavajući prvu transakciju koja je potrošila novčić. Potrebna je prednost prirode informacije koju je lako širiti, ali je teško ugušiti. Za detalje o tome kako to funkcioniše, pogledajte članak o dizajnu na bitcoin.org

Satoshi Nakamoto

Koje Probleme Rešava Bitcoin?

Razdvojimo neke od Satoshi-jevih postova kako bismo uvideli razloge njegove motivacije.

„Razvio sam novi P2P sistem e-keša otvorenog koda.“

P2P je skraćenica za peer to peer i ukazuje na sistem u kojem jedna osoba može da komunicira sa drugom bez ikoga u sredini, kao medjusobno jednaki.

Možete se setiti P2P tehnologija za razmenu datoteka poput Napster-a, Kazaa-e i BitTorrrent-a, koje su prve omogućile ljudima da dele muziku i filmove bez posrednika.

Satoshi je dizajnirao Bitcoin kako bi omogućio ljudima da razmenjuju e-keš, elektronski keš, bez prolaska preko posrednika na približno isti način.

Softver je otvorenog koda, što znači da svako može videti kako funkcioniše i doprineti tome.

Ne treba da verujemo ni u šta što je Satoshi napisao u svom postu o tome kako softver radi.

Možemo pogledati kod i sami proveriti kako to funkcioniše. Štaviše, možemo promeniti funkcionalnost sistema promenom koda.

„Potpuno je decentralizovan, bez centralnog servera ili pouzdanih stranki …“

Satoshi napominje da je sistem decentralizovan kako bi se razlikovao od sistema koji imaju centralnu kontrolu.

Prethodne pokušaje stvaranja digitalne gotovine poput DigiCash-a od strane Davida Chaum-a podržavao je centralni server, računar ili skup računara koji je bio odgovoran za izdavanje i verifikaciju plaćanja pod kontrolom jedne korporacije.

Takve, centralno kontrolisane privatne šeme novca, bile su osuđene na propast; ljudi se ne mogu osloniti na novac koji može nestati kada kompanija prestane sa poslovanjem, bude hakovana, pretrpi pad servera ili je zatvori vlada.

Bitcoin održava mreža pojedinaca i kompanija širom sveta.

Da bi se Bitcoin isključio, bilo bi potrebno isključiti desetine do stotine hiljada računara širom sveta u isto vreme, zauvek, od kojih su mnogi na nepoznatim lokacijama.

Bila bi to beznadežna igra, jer bi svaki napad ove prirode jednostavno podstakao stvaranje novih Bitcoin čvorova ili računara na mreži.

„… sve se zasniva na kripto dokazima umesto na poverenju“

Internet, a u stvari i većina savremenih računarskih sistema, izgrađeni su na kriptografiji, metodi prikrivanja informacija, tako da je može dekodirati samo primalac informacije.

Kako se Bitcoin oslobađa potrebe za poverenjem? Umesto da verujemo nekome ko kaže „Ja sam Alisa“ ili „Imam 10 $ na računu“, možemo koristiti kriptografsku matematiku da bismo izneli iste činjenice na način koji je vrlo lako verifikovati od strane primaoca dokaza ali ga je nemoguće falsifikovati.

Bitcoin u svom dizajnu koristi kriptografsku matematiku kako bi učesnicima omogućio da provere ponašanje svih ostalih učesnika, bez poverenja u bilo koju centralnu stranku.

„Moramo im verovati [bankama] sa našom privatnošću, verovati im da neće dozvoliti da kradljivci identiteta pokradu naše račune“

Za razliku od korišćenja vašeg bankovnog računa, sistema digitalnog plaćanja ili kreditne kartice, Bitcoin omogućava dvema stranama da obavljaju transakcije bez davanje bilo kakvih ličnih podataka.

Centralizovana skladišta potrošačkih podataka koji se čuvaju u bankama, kompanijama sa kreditnim karticama, procesorima plaćanja i vladama, predstavljaju pravu poslasticu za hakere.

Kao dokaz Satoshi-jeve poente služi primer iz 2017. godine kada je Equifax masovono kompromitovan, kada su hakeri ukrali identifikacione i finansijske podatke za više od 140 miliona ljudi.

Bitcoin odvaja finansijske transakcije od stvarnih identiteta.

Na kraju krajeva, kada nekome damo fizički novac, on nema potrebu da zna ko smo, niti treba da brinemo da će nakon naše razmene moći da iskoristi neke informacije koje smo mu dali da ukrade još našeg novca.

Zašto ne bismo očekivali isto, ili čak i bolje, od digitalnog novca?

„Centralnoj banci se mora verovati da neće devalvirati valutu, ali istorija tradicionalnih valuta je puna primera kršenja tog poverenja.“

Pojam tradicionalna valuta, odnosi se na valutu izdatu od strane vlade i centralne banke, koju vlada proglašava zakonskim sredstvom plaćanja.

Istorijski, novac je nastao od stvari koje je bilo teško proizvesti, koje su bile lake za proveravanje i transport, poput školjki, staklenih perli, srebra i zlata.

Kad god bi se nešto koristilo kao novac, postojalo je iskušenje da se stvori više toga.

Ako bi neko pronašao vrhunsku tehnologiju za brzo stvaranje velike količine nečega, ta stvar bi izgubila vrednost.

Evropski naseljenici uspeli su da liše afrički kontinent bogatstva trgujući staklenim perlicama koje su se lako proizvodile za ljudske robove.

Isto se dogodilo sa američkim indijancima, kada su kolonisti otkrili način brze proizvodnje vampum školjki, koje su starosedeoci smatrali retkim.

Vremenom, širom sveta ljudi su shvatili da je samo zlato dovoljno retko da deluje kao novac, bez straha da bi neko drugi mogao da ga stvori u velikim količinama.

Polako smo prešli sa svetske ekonomije koja je koristila zlato kao novac na onu gde su banke izdavale papirne sertifikate kao dokaz posedovanja tog zlata.

Nixon je okončao međunarodnu konvertibilnost američkog dolara u zlato 1971. godine, privremenim rešenjem, koje je ubrzo postalo trajno.

Kraj zlatnog standarda omogućio je vladama i centralnim bankama da imaju punu dozvolu da povećavaju novčanu masu po svojoj volji, razredjujući vrednost svake novčanice u opticaju, poznatije kao umanjenje vrednosti.

Iako je izdata od strane vlade, suštinska tradicionalna valuta je novac koji svi znamo i svakodnevno koristimo, ipak je relativno novo iskustvo u opsegu svetske istorije.

Moramo verovati našim vladama da ne zloupotrebljavaju njegovo štamparije, i ne treba nam puno muke da nadjemo primere kršenja tog poverenja.

U autokratskim i centralno planiranim režimima gde vlada ima prst direktno na mašini za novac, kao što je Venecuela, valuta je postala gotovo bezvredna.

Venecuelanski Bolivar prešao je sa 2 bolivara za 1 američki dolar, koliko je vredeo 2009. godine, na 250.000 bolivara za 1 američki dolar 2019. godine.

Pogledajte koliko novčanica je bilo potrebno za kupovinu piletine u Venecueli posle hiperinflacije.

Satoshi je želeo da ponudi alternativu tradicionalnoj valuti čija se ponuda uvek nepredvidivo širi.

Da bi sprečilo umanjenje vrednosti, Satoshi je dizajnirao novčani sistem gde je zaliha bila fiksna i izdavana po predvidljivoj i nepromenjivoj stopi.

Postojaće samo 21 milion Bitcoin-a.

Međutim, svaki Bitcoin se može podeliti na 100 miliona jedinica koje se sada nazivaju satoshis (sats-ovi), što će činiti ukupno 2,1 kvadriliona satoshi-a u opticaju oko 2140. godine.

Pre Bitcoin-a nije bilo moguće sprečiti beskrajnu reprodukciju digitalnih sredstava.

Kopirati digitalnu knjigu, audio datoteku ili video zapis i poslati ga prijatelju, je jeftino i lako.

Jedini izuzeci od toga su digitalna sredstva koja kontrolišu posrednici.

Na primer, kada iznajmite film sa iTunes-a, možete ga gledati na vašem uređaju samo zato što iTunes kontroliše distribuciju tog filma i može ga zaustaviti nakon perioda njegovog iznajmljivanja.

Slično tome, vaša banka kontroliše vaš digitalni novac. Zadatak banke je da vodi evidenciju koliko novca imate.

Ako ga prenesete nekom drugom, oni će odobriti ili odbiti takav prenos.

Bitcoin je prvi digitalni sistem koji sprovodi oskudicu bez posrednika i prvo je sredstvo poznato čovečanstvu čija je nepromenljiva ponuda i raspored izdavanja poznat unapred.

Ni plemeniti metali poput zlata nemaju ovo svojstvo, jer uvek možemo iskopati sve više i više zlata ukoliko je to isplativo.

Zamislite da otkrijemo asteroid koji sadrži deset puta više zlata nego što ga imamo na zemlji.

Šta bi se dogodilo sa cenom zlata uzimajući u obzir tako obilnu ponudu? Bitcoin je imun na takva otkrića i manipulisanje nabavkom.

Jednostavno je nemoguće proizvesti više od toga (21 miliona).

„Podaci bi se mogli osigurati na način koji je fizički bio nemoguć za pristup drugima, bez obzira iz kog razloga, bez obzira koliko je dobar izgovor, bez obzira na sve. […] Vreme je da imamo istu stvar za novac “

Naše trenutne metode obezbeđivanja novca, poput stavljanja u banku, oslanjaju se na poverenje nekome drugom da će obaviti taj posao.

Poverenje u takvog posrednika ne zahteva samo sigurnost da on neće učiniti nešto zlonamerno ili glupo, već i da vlada neće zapleniti ili zamrznuti vaša sredstva vršeći pritisak na ovog posrednika.

Međutim, videli smo bezbroj puta da vlade mogu, i zaista uskraćuju pristup novcu kada se osećaju ugroženo.

Nekom ko živi u Sjedinjenim Državama ili nekoj drugoj visoko regulisanoj ekonomiji možda zvuči glupo da razmišlja da se probudi sa oduzetim novcem, ali to se događa stalno.

PayPal mi je zamrzao sredstva jednostavno zato par meseci nisam koristio svoj račun.

Trebalo mi je više od nedelju dana da vratim pristup „svom“ novcu.

Srećan sam što živim u Europi, gde bih se bar mogao nadati da ću potražiti neko pravno rešenje ako mi PayPal zamrzne sredstva i gde imam osnovno poverenje da moja vlada i banka neće ukrasti moj novac.

Mnogo gore stvari su se dogodile, i trenutno se dešavaju, u zemljama sa manje slobode.

Banke su se zatvorile tokom kolapsa valuta u Grčkoj.

Banke na Kipru su koristile kaucije da konfiskuju sredstva od svojih klijenata.

Indijska vlada je proglasila određene novčanice bezvrednim.

Bivši SSSR, u kojem sam odrastao, imao je ekonomiju pod kontrolom vlade što je dovelo do ogromnih nestašica robe.

Bilo je nezakonito posedovati strane valute kao što je američki dolar.

Kada smo poželeli da odemo, mojoj porodici je bilo dozvoljeno da zameni samo ograničenu količinu novca po osobi za američke dolare po zvaničnom kursu koji je bio u velikoj meri različit od pravog kursa slobodnog tržišta.

U stvari, vlada nam je oduzela ono malo bogatstva koje smo imali koristeći gvozdeni stisak na ekonomiji i kretanju kapitala.

Autokratske zemlje imaju tendenciju da sprovode strogu ekonomsku kontrolu, sprečavajući ljude da na slobodnom tržištu povuku svoj novac iz banaka, iznesu ga iz zemlje ili da ga razmene u ne još uvek bezvredne valute poput američkog dolara.

To omogućava vladinoj slobodnoj vladavini da primeni sulude ekonomske eksperimente poput socijalističkog sistema SSSR-a.

Bitcoin se ne oslanja na poverenje u treću stranu da bi osigurao vaš novac.

Umesto toga, Bitcoin onemogućava drugima pristup vašim novčićima bez jedinstvenog ključa koji imate samo vi, bez obzira iz kog razloga, bez obzira koliko je dobar izgovor, bez obzira na sve.

Držeći Bitcoin, držite ključeve sopstvene finansijske slobode. Bitcoin razdvaja novac i državu

„Rešenje Bitcoin-a je korišćenje peer-to-peer mreže za proveru dvostruke potrošnje […] poput distribuiranog servera vremenskih žigova, obeležavajući prvu transakciju koja je potrošila novčić“

Mreža se odnosi na ideju da je gomila računara povezana i da mogu međusobno slati poruke.

Reč distribuirano znači da ne postoji centralna stranka koja kontroliše, već da svi učesnici koordiniraju medjusobno kako bi mreža bila uspešna.

U sistemu bez centralne kontrole, bitno je znati da niko ne vara. Ideja dvostruke potrošnje odnosi se na mogućnost trošenja istog novca dva puta.

Fizički novac odlazi iz vaše ruke kad ga potrošite. Međutim, digitalne transakcije se mogu kopirati baš kao muzika ili filmovi.

Kada novac šaljete preko banke, oni se pobrinu da isti novac ne možete da prebacujete dva puta.

U sistemu bez centralne kontrole potreban nam je način da sprečimo ovu vrstu dvostruke potrošnje, koja je u suštini ista kao i falsifikovanje novca.

Satoshi opisuje da učesnici u Bitcoin mreži rade zajedno kako bi vremenski označili (doveli u red) transakcije kako bismo znali šta je bilo prvo.

Zbog toga možemo odbiti sve buduće pokušaje trošenja istog novca.

Satoshi se uhvatio u koštac sa nekoliko zanimljivih tehničkih problema kako bi rešio probleme privatnosti, uništavanja vrednosti i centralne kontrole u trenutnim monetarnim sistemima.

Na kraju je stvorio peer to peer mrežu kojoj se svako mogao pridružiti bez otkrivanja svog identiteta ili potrebe da veruje bilo kom drugom učesniku.

Kako se Bitcoin razvijao u poslednjoj deceniji?

Doprinosi izvornom kodu Bitcoina

Kada je Bitcoin pokrenut, samo nekolicina ljudi ga je koristila i pokrenula Bitcoin softver na svojim računarima za napajanje Bitcoin mreže.

Većina ljudi u to vreme mislila je da je to šala ili da će se otkriti ozbiljni nedostaci u dizajnu sistema koji će ga učiniti neizvodljivim.

Vremenom se mreži pridružilo sve više ljudi koji su pomoću svojih računara dodali sigurnost mreži.

Ljudi su počeli da menjaju Bitcoin-e za robu i usluge, dajući mu stvarnu vrednost. Pojavile su se menjačnice valuta koje su menjale Bitcoin-e za gotovo sve tradicionalne valute na svetu.

Deset godina nakon izuma, Bitcoin koriste milioni ljudi sa desetinama do stotinama hiljada čvorova koji pokreću besplatni Bitcoin softver, koji se razvija od strane stotina dobrovoljaca i kompanija širom sveta.

Bitcoin mreža je porasla kako bi obezbedila vrednost veću od stotine biliona dolara.

Računari koji učestvuju u zaštiti Bitcoin mreže poznati su kao rudari/majneri.

Oni rade u industrijskim operacijama širom sveta, ulažući milione dolara u specijalni rudarski hardver koji radi samo jedno: pobrinuti se da je Bitcoin najsigurnija mreža na planeti.

Rudari troše električnu energiju kako bi transakcije Bitcoin-a učinile sigurnim od modifikacija. Budući da se rudari međusobno takmiče za oskudan broj Bitcoin-a proizvedenih dnevno, oni uvek moraju da pronalaze najjeftinije izvore energije na planeti da bi ostali profitabilni.

Rudari rade na različitim mestima, od hidroelektrana u dalekim krajevima Kine do vetroparkova u Teksasu, do kanadskih naftnih polja koja proizvode gas koji bi u suprotnom bio odzračen ili spaljen u atmosferi.

Iako je Bitcoin popularna tema i o njemu se često raspravlja u medijima, procenjujemo da je samo nekoliko miliona ljudi na svetu počelo da redovno štedi Bitcoin.

Za mnoge ljude, posebno za one koji nikada nisu živeli pod represivnim režimima, ovaj izum novog oblika digitalnog novca izvan kontrole vlade može biti veoma izazovan za razumevanje i prihvatanje.

Zato sam ja ovde. Želim da vam pomognem da razumete Bitcoin i budete gospodar svoje budućnosti!

-

@ 0e9491aa:ef2adadf

2025-05-24 17:01:16

For years American bitcoin miners have argued for more efficient and free energy markets. It benefits everyone if our energy infrastructure is as efficient and robust as possible. Unfortunately, broken incentives have led to increased regulation throughout the sector, incentivizing less efficient energy sources such as solar and wind at the detriment of more efficient alternatives.

The result has been less reliable energy infrastructure for all Americans and increased energy costs across the board. This naturally has a direct impact on bitcoin miners: increased energy costs make them less competitive globally.

Bitcoin mining represents a global energy market that does not require permission to participate. Anyone can plug a mining computer into power and internet to get paid the current dynamic market price for their work in bitcoin. Using cellphone or satellite internet, these mines can be located anywhere in the world, sourcing the cheapest power available.

Absent of regulation, bitcoin mining naturally incentivizes the build out of highly efficient and robust energy infrastructure. Unfortunately that world does not exist and burdensome regulations remain the biggest threat for US based mining businesses. Jurisdictional arbitrage gives miners the option of moving to a friendlier country but that naturally comes with its own costs.

Enter AI. With the rapid development and release of AI tools comes the requirement of running massive datacenters for their models. Major tech companies are scrambling to secure machines, rack space, and cheap energy to run full suites of AI enabled tools and services. The most valuable and powerful tech companies in America have stumbled into an accidental alliance with bitcoin miners: THE NEED FOR CHEAP AND RELIABLE ENERGY.

Our government is corrupt. Money talks. These companies will push for energy freedom and it will greatly benefit us all.

Microsoft Cloud hiring to "implement global small modular reactor and microreactor" strategy to power data centers: https://www.datacenterdynamics.com/en/news/microsoft-cloud-hiring-to-implement-global-small-modular-reactor-and-microreactor-strategy-to-power-data-centers/

If you found this post helpful support my work with bitcoin.

-

@ eb0157af:77ab6c55

2025-05-24 17:01:12

The exchange reveals the extent of the breach that occurred last December as federal authorities investigate the recent data leak.

Coinbase has disclosed that the personal data of 69,461 users was compromised during the breach in December 2024, according to documentation filed with the Maine Attorney General’s Office.

The disclosure comes after Coinbase announced last week that a group of hackers had demanded a $20 million ransom, threatening to publish the stolen data on the dark web. The attackers allegedly bribed overseas customer service agents to extract information from the company’s systems.

Coinbase had previously stated that the breach affected less than 1% of its user base, compromising KYC (Know Your Customer) data such as names, addresses, and email addresses. In a filing with the U.S. Securities and Exchange Commission (SEC), the company clarified that passwords, private keys, and user funds were not affected.

Following the reports, the SEC has reportedly opened an official investigation to verify whether Coinbase may have inflated user metrics ahead of its 2021 IPO. Separately, the Department of Justice is investigating the breach at Coinbase’s request, according to CEO Brian Armstrong.

Meanwhile, Coinbase has faced criticism for its delayed response to the data breach. Michael Arrington, founder of TechCrunch, stated that the stolen data could cause irreparable harm. In a post on X, Arrington wrote:

“The human cost, denominated in misery, is much larger than the $400m or so they think it will actually cost the company to reimburse people. The consequences to companies who do not adequately protect their customer information should include, without limitation, prison time for executives.”

Coinbase estimates the incident could cost between $180 million and $400 million in remediation expenses and customer reimbursements.

Arrington also condemned KYC laws as ineffective and dangerous, calling on both regulators and companies to better protect user data:

“Combining these KYC laws with corporate profit maximization and lax laws on penalties for hacks like these means these issues will continue to happen. Both governments and corporations need to step up to stop this. As I said, the cost can only be measured in human suffering.”

The post Coinbase: 69,461 users affected by December 2024 data breach appeared first on Atlas21.

-

@ dfa02707:41ca50e3

2025-05-24 17:00:56

Contribute to keep No Bullshit Bitcoin news going.

News

- Spiral welcomes Ben Carman. The developer will work on the LDK server and a new SDK designed to simplify the onboarding process for new self-custodial Bitcoin users.

- Spiral renews support for Dan Gould and Joschisan. The organization has renewed support for Dan Gould, who is developing the Payjoin Dev Kit (PDK), and Joschisan, a Fedimint developer focused on simplifying federations.

- The Bitcoin Dev Kit Foundation announced new corporate members for 2025, including AnchorWatch, CleanSpark, and Proton Foundation. The annual dues from these corporate members fund the small team of open-source developers responsible for maintaining the core BDK libraries and related free and open-source software (FOSS) projects.

- The European Central Bank is pushing for amendments to the European Union's Markets in Crypto Assets legislation (MiCA), just months after its implementation. According to Politico's report on Tuesday, the ECB is concerned that U.S. support for cryptocurrency, particularly stablecoins, could cause economic harm to the 27-nation bloc.

- Slovenia is considering a 25% capital gains tax on Bitcoin profits for individuals. The Ministry of Finance has proposed legislation to impose this tax on gains from cryptocurrency transactions, though exchanging one cryptocurrency for another would remain exempt. At present, individual 'crypto' traders in Slovenia are not taxed.

- The Virtual Asset Service Providers (VASP) Bill 2025 introduced in Kenya. The new legislation aims to establish a comprehensive legal framework for licensing, regulating, and supervising virtual asset service providers (VASPs), with strict penalties for non-compliant entities.

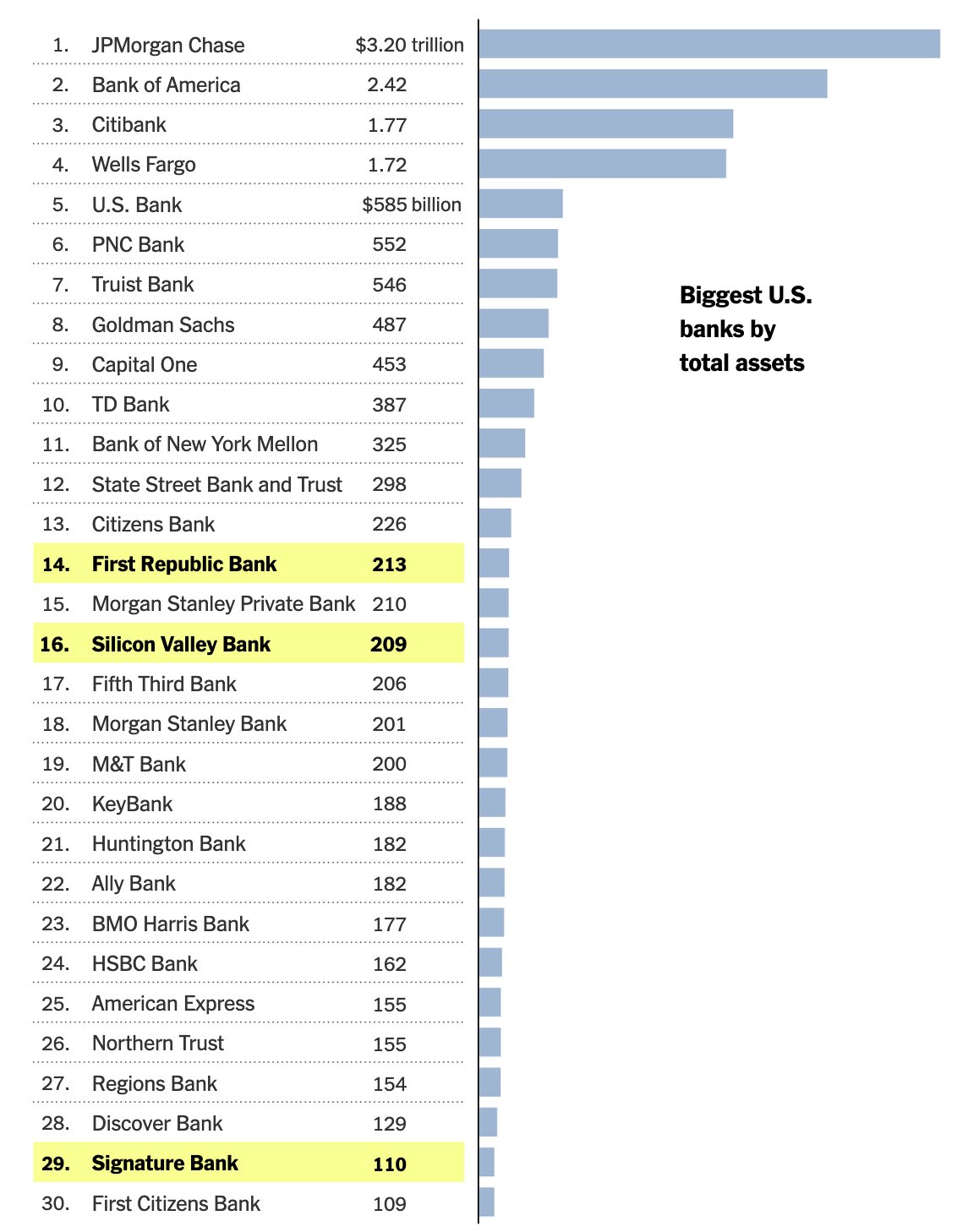

- Circle, BitGo, Coinbase, and Paxos plan to apply for U.S. bank charters or licenses. According to a report in The Wall Street Journal, major crypto companies are planning to apply for U.S. bank charters or licenses. These firms are pursuing limited licenses that would permit them to issue stablecoins, as the U.S. Congress deliberates on legislation mandating licensing for stablecoin issuers.

"Established banks, like Bank of America, are hoping to amend the current drafts of [stablecoin] legislation in such a way that nonbanks are more heavily restricted from issuing stablecoins," people familiar with the matter told The Block.

- Paul Atkins has officially assumed the role of the 34th Chairman of the US Securities and Exchange Commission (SEC). This is a return to the agency for Atkins, who previously served as an SEC Commissioner from 2002 to 2008 under the George W. Bush administration. He has committed to advancing the SEC’s mission of fostering capital formation, safeguarding investors, and ensuring fair and efficient markets.

- Federal Reserve retracts guidance discouraging banks from engaging in 'crypto.' The U.S. Federal Reserve withdrew guidance that discouraged banks from crypto and stablecoin activities, as announced by its Board of Governors on Thursday. This includes rescinding a 2022 supervisory letter requiring prior notification of crypto activities and 2023 stablecoin requirements.

"As a result, the Board will no longer expect banks to provide notification and will instead monitor banks' crypto-asset activities through the normal supervisory process," reads the FED statement.

- Russian government to launch a cryptocurrency exchange. The country's Ministry of Finance and Central Bank announced plans to establish a trading platform for "highly qualified investors" that "will legalize crypto assets and bring crypto operations out of the shadows."

- Twenty One Capital is set to launch with over 42,000 BTC in its treasury. This new Bitcoin-native firm, backed by Tether and SoftBank, is planned to go public via a SPAC merger with Cantor Equity Partners and will be led by Jack Mallers, co-founder and CEO of Strike. According to a report by the Financial Times, the company aims to replicate the model of Michael Saylor with his company, MicroStrategy.

- Strategy increases Bitcoin holdings to 538,200 BTC. In the latest purchase, the company has spent more than $555M to buy 6,556 coins through proceeds of two at-the-market stock offering programs.

- Metaplanet buys another 145 BTC. The Tokyo-listed company has purchased an additional 145 BTC for $13.6 million. Their total bitcoin holdings now stand at 5,000 coins, worth around $428.1 million.

- Semler Scientific has increased its bitcoin holdings to 3,303 BTC. The company acquired an additional 111 BTC at an average price of $90,124. The purchase was funded through proceeds from an at-the-market offering and cash reserves, as stated in a press release.

- Tesla still holds nearly $1 billion in bitcoin. According to the automaker's latest earnings report, the firm reported digital asset holdings worth $951 million as of March 31.

- Spar supermarket experiments with Bitcoin payments in Zug, Switzerland. The store has introduced a new payment method powered by the Lightning Network. The implementation was facilitated by DFX Swiss, a service that supports seamless conversions between bitcoin and legacy currencies.

- Charles Schwab to launch spot Bitcoin trading by 2026. The financial investment firm, managing over $10 trillion in assets, has revealed plans to introduce spot Bitcoin trading for its clients within the next year.

- Arch Labs has secured $13 million to develop "ArchVM" and integrate smart-contract functionality with Bitcoin. The funding round, valuing the company at $200 million, was led by Pantera Capital, as announced on Tuesday.

- Citrea deployed its Clementine Bridge on the Bitcoin testnet. The bridge utilizes the BitVM2 programming language to inherit validity from Bitcoin, allegedly providing "the safest and most trust-minimized way to use BTC in decentralized finance."

- UAE-based Islamic bank ruya launches Shari’ah-compliant bitcoin investing. The bank has become the world’s first Islamic bank to provide direct access to virtual asset investments, including Bitcoin, via its mobile app, per Bitcoin Magazine.

- Solosatoshi.com has sold over 10,000 open-source miners, adding more than 10 PH of hashpower to the Bitcoin network.

"Thank you, Bitaxe community. OSMU developers, your brilliance built this. Supporters, your belief drives us. Customers, your trust powers 10,000+ miners and 10PH globally. Together, we’re decentralizing Bitcoin’s future. Last but certainly not least, thank you@skot9000 for not only creating a freedom tool, but instilling the idea into thousands of people, that Bitcoin mining can be for everyone again," said the firm on X.

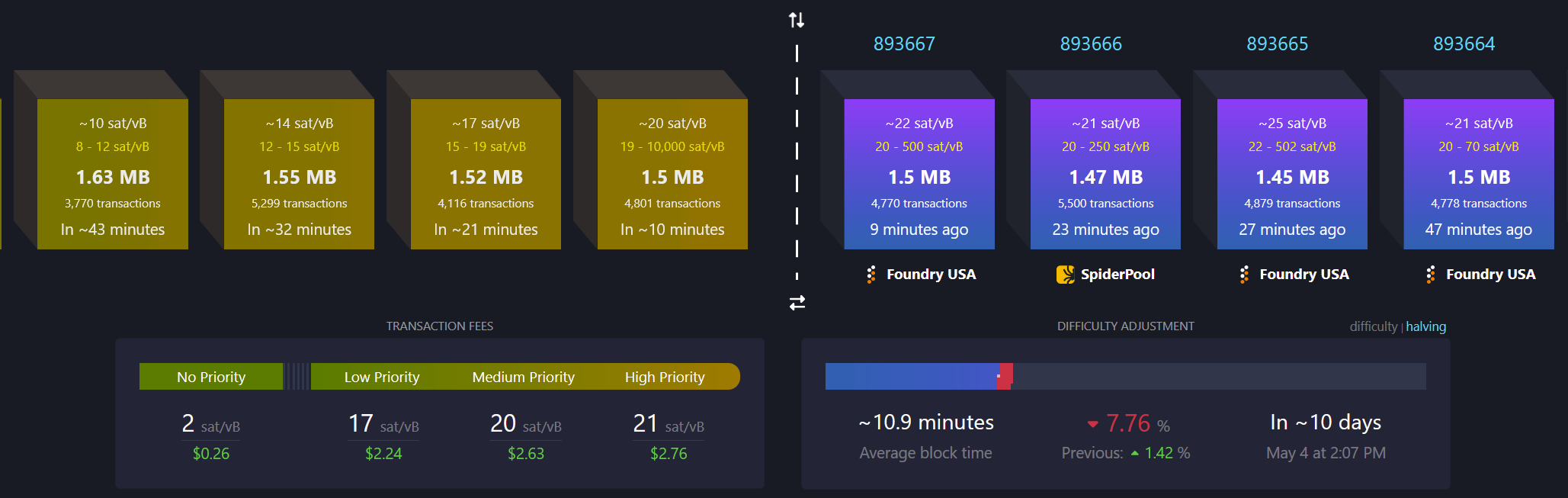

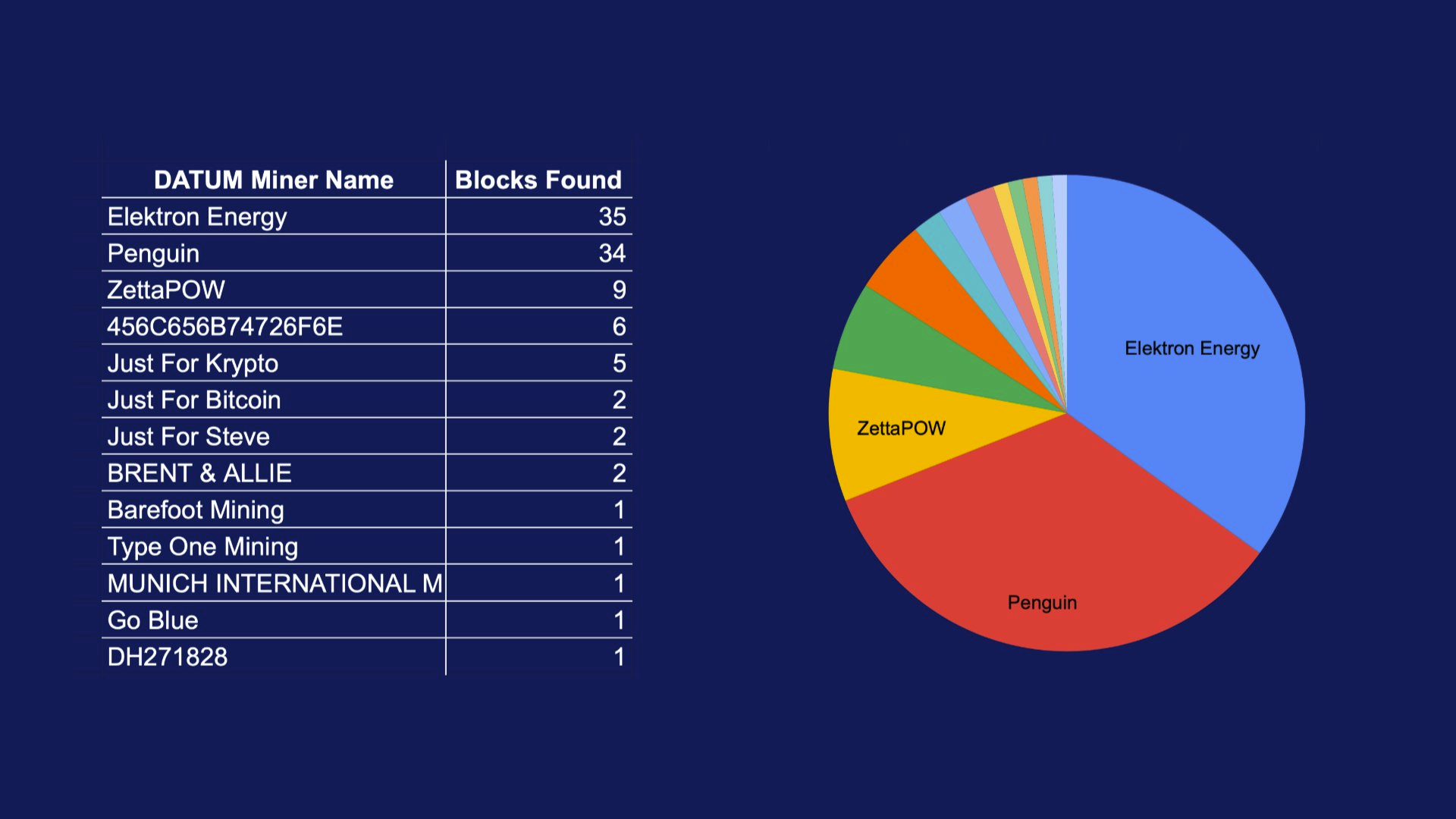

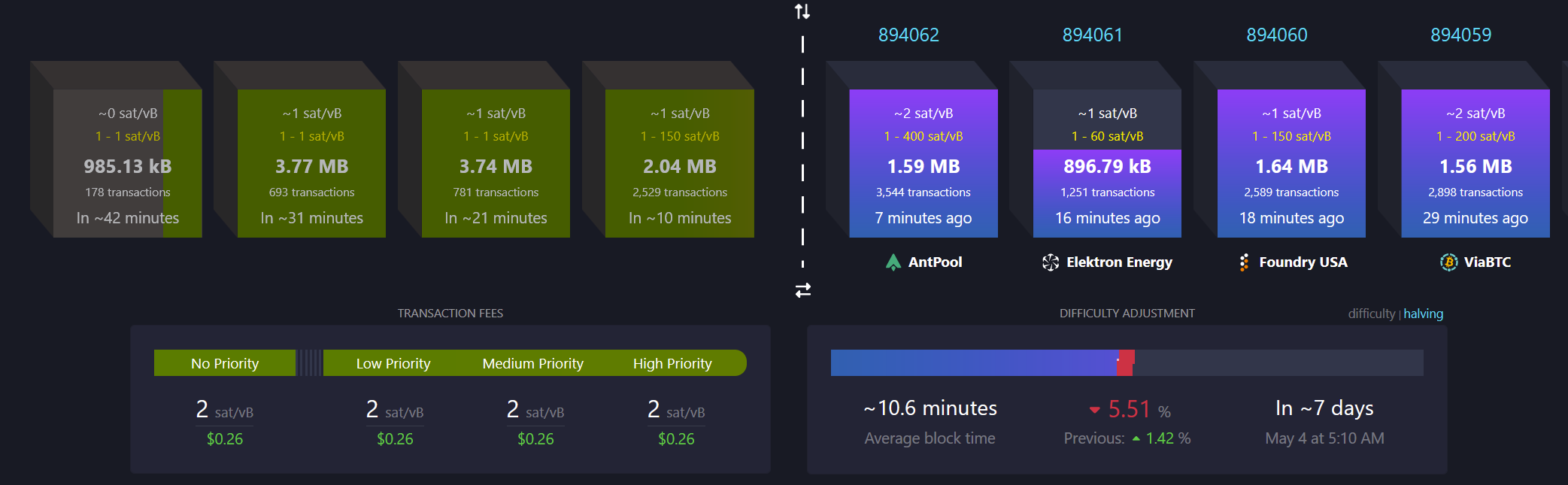

- OCEAN's DATUM has found 100 blocks. "Over 65% of OCEAN’s miners are using DATUM, and that number is growing every day. This means block template construction is making its way back into the hands of the miners, which is not only the most profitable

-

@ b1ddb4d7:471244e7

2025-05-24 17:00:36

Flash, an all-in-one Bitcoin payment platform, has announced the launch of Flash 2.0, the most intuitive and powerful Bitcoin payment solution to date.

With a completely redesigned interface, expanded e-commerce integrations, and a frictionless onboarding process, Flash 2.0 makes accepting Bitcoin easier than ever for businesses worldwide.

We did the unthinkable!

We did the unthinkable! Website monetization used to be super complicated.

"Buy me a coffee" — But only if we both have a bank account.

WHAT IF WE DON'T?

Thanks to @paywflash and bitcoin, it's just 5 CLICKS – and no banks!

Start accepting donations on your website… pic.twitter.com/uwZUrvmEZ1

Start accepting donations on your website… pic.twitter.com/uwZUrvmEZ1— Flash • The Bitcoin Payment Gateway (@paywflash) May 13, 2025

Accept Bitcoin in Three Minutes

Setting up Bitcoin payments has long been a challenge for merchants, requiring technical expertise, third-party processors, and lengthy verification procedures. Flash 2.0 eliminates these barriers, allowing any business to start accepting Bitcoin in just three minutes, with no technical set-up and full control over their funds.

The Bitcoin Payment Revolution

The world is witnessing a seismic shift in finance. Governments are backing Bitcoin funds, major companies are adding Bitcoin to their balance sheets, and political figures are embracing it as the future of money. Just as Stripe revolutionized internet payments, Flash is now doing the same for Bitcoin. Businesses that adapt today will gain a competitive edge in a rapidly evolving financial landscape.

With Bitcoin adoption accelerating, consumers are looking for places to spend it. Flash 2.0 ensures businesses of all sizes can seamlessly accept Bitcoin and position themselves at the forefront of this financial revolution.

All-in-One Monetization Platform

More than just a payment gateway, Flash 2.0 is a complete Bitcoin monetization suite, providing multiple ways for businesses to integrate Bitcoin into their operations. Merchants can accept payments online and in-store, content creators can monetize with donations and paywalls, and freelancers can send instant invoices via payment links.

For example, a jewelry designer selling products on WooCommerce can now integrate Flash for online payments, use Flash’s Point-of-Sale system at trade shows, enable Bitcoin donations for her digital artwork, and lock premium content behind Flash Paywalls. The possibilities are endless.

E-Commerce for Everyone

With built-in integrations for Shopify, WooCommerce, and soon Wix and OpenCart, Flash 2.0 enables Bitcoin payments on 95% of e-commerce stores worldwide. Businesses can now add Bitcoin as a payment option in just a few clicks—without needing developers or external payment processors.

And for those looking to start selling, Flash’s built-in e-commerce features allow users to create online stores, showcase products, and manage payments seamlessly.

No Middlemen, No Chargebacks, No Limits

Unlike traditional payment platforms, Flash does not hold or process funds. Businesses receive Bitcoin directly, instantly, and securely. There are no chargebacks, giving merchants full control over refunds and eliminating fraud. Flash also remains KYC-free, ensuring a seamless experience for businesses and customers alike.

A Completely Redesigned Experience

“The world is waking up to Bitcoin. Just like the internet revolutionized commerce, Bitcoin is reshaping finance. Businesses need solutions that are simple, efficient, and truly decentralized. Flash 2.0 is more than just a payment processor—it’s a gateway to the future of digital transactions, putting financial power back into the hands of businesses.”

— Pierre Corbin, CEO at Flash.

Flash 2.0 introduces a brand-new user interface, making it easier than ever to navigate, set up payments, and manage transactions. With an intuitive dashboard, streamlined checkout, and enhanced mobile compatibility, the platform is built for both new and experienced Bitcoin users.

About Flash

Flash is an all-in-one Bitcoin payment platform that empowers businesses, creators, and freelancers to accept, manage, and grow with Bitcoin. With a mission to make Bitcoin payments accessible to everyone, Flash eliminates complexity and gives users full control over their funds.

To learn more or get started, visit www.paywithflash.com.

Press Contact:

Julien Bouvier

Head of Marketing

+3360941039 -

@ b1ddb4d7:471244e7

2025-05-24 17:00:34

Bitcoin FilmFest (BFF25) returns to Warsaw for its third edition, blending independent cinema—from feature films and commercials to AI-driven experimental visuals—with education and entertainment.

Hundreds of attendees from around the world will gather for three days of screenings, discussions, workshops, and networking at the iconic Kinoteka Cinema (PKiN), the same venue that hosted the festival’s first two editions in March 2023 and April 2024.

This year’s festival, themed “Beyond the Frame,” introduces new dimensions to its program, including an extra day on May 22 to celebrate Bitcoin Pizza Day, the first real-world bitcoin transaction, with what promises to be one of Europe’s largest commemorations of this milestone.

BFF25 bridges independent film, culture, and technology, with a bold focus on decentralized storytelling and creative expression. As a community-driven cultural experience with a slightly rebellious spirit, Bitcoin FilmFest goes beyond movies, yet cinema remains at its heart.

Here’s a sneak peek at the lineup, specially curated for movie buffs:

Generative Cinema – A special slot with exclusive shorts and a thematic debate on the intersection of AI and filmmaking. Featured titles include, for example: BREAK FREE, SATOSHI: THE CREATION OF BITCOIN, STRANGE CURRENCIES, and BITCOIN IS THE MYCELIUM OF MONEY, exploring financial independence, traps of the fiat system, and a better future built on sound money.

Generative Cinema – A special slot with exclusive shorts and a thematic debate on the intersection of AI and filmmaking. Featured titles include, for example: BREAK FREE, SATOSHI: THE CREATION OF BITCOIN, STRANGE CURRENCIES, and BITCOIN IS THE MYCELIUM OF MONEY, exploring financial independence, traps of the fiat system, and a better future built on sound money. Upcoming Productions Preview – A bit over an hour-long block of unreleased pilots and works-in-progress. Attendees will get exclusive first looks at projects like FINDING HOME (a travel-meets-personal-journey series), PARALLEL SPACES (a story about alternative communities), and THE LEGEND OF LANDI (a mysterious narrative).

Upcoming Productions Preview – A bit over an hour-long block of unreleased pilots and works-in-progress. Attendees will get exclusive first looks at projects like FINDING HOME (a travel-meets-personal-journey series), PARALLEL SPACES (a story about alternative communities), and THE LEGEND OF LANDI (a mysterious narrative). Freedom-Focused Ads & Campaigns – Unique screenings of video commercials, animations, and visual projects, culminating in “The PoWies” (Proof of Work-ies)—the first ever awards show honoring the best Bitcoin-only awareness campaigns.

Freedom-Focused Ads & Campaigns – Unique screenings of video commercials, animations, and visual projects, culminating in “The PoWies” (Proof of Work-ies)—the first ever awards show honoring the best Bitcoin-only awareness campaigns.To get an idea of what might come up at the event, here, you can preview 6 selected ads combined into two 2 videos:

Open Pitch Competition – A chance for filmmakers to present fresh ideas and unfinished projects to an audience of a dedicated jury, movie fans and potential collaborators. This competitive block isn’t just entertaining—it’s a real opportunity for creators to secure funding and partnerships.

Open Pitch Competition – A chance for filmmakers to present fresh ideas and unfinished projects to an audience of a dedicated jury, movie fans and potential collaborators. This competitive block isn’t just entertaining—it’s a real opportunity for creators to secure funding and partnerships. Golden Rabbit Awards: A lively gala honoring films from the festival’s Official Selection, with awards in categories like Best Feature, Best Story, Best Short, and Audience Choice.

Golden Rabbit Awards: A lively gala honoring films from the festival’s Official Selection, with awards in categories like Best Feature, Best Story, Best Short, and Audience Choice.BFF25 Main Screenings

Sample titles from BFF25’s Official Selection:

REVOLUCIÓN BITCOIN – A documentary by Juan Pablo, making its first screening outside the Spanish-speaking world in Warsaw this May. Three years of important work, 80 powerful minutes to experience. The film explores Bitcoin’s impact across Argentina, Colombia, Mexico, El Salvador, and Spain through around 40 diverse perspectives. Screening in Spanish with English subtitles, followed by a Q&A with the director. UNBANKABLE – Luke Willms’ directorial debut, drawing from his multicultural roots and his father’s pioneering HIV/AIDS research. An investigative documentary based on Luke’s journeys through seven African countries, diving into financial experiments and innovations—from mobile money and digital lending to Bitcoin—raising smart questions and offering potential lessons for the West. Its May appearance at BFF25 marks its largest European event to date, following festival screenings and nominations across multiple continents over the past year. HOTEL BITCOIN – A Spanish comedy directed by Manuel Sanabria and Carlos “Pocho” Villaverde. Four friends, 4,000 bitcoins , and one laptop spark a chaotic adventure of parties, love, crime, and a dash of madness. Exploring sound money, value, and relationships through a twisting plot. The film premiered at the Tarazona and Moncayo Comedy Film Festival in August 2024. Its Warsaw screening at BFF25 (in Spanish with English subtitles) marks its first public showing outside the Spanish-speaking world.

REVOLUCIÓN BITCOIN – A documentary by Juan Pablo, making its first screening outside the Spanish-speaking world in Warsaw this May. Three years of important work, 80 powerful minutes to experience. The film explores Bitcoin’s impact across Argentina, Colombia, Mexico, El Salvador, and Spain through around 40 diverse perspectives. Screening in Spanish with English subtitles, followed by a Q&A with the director. UNBANKABLE – Luke Willms’ directorial debut, drawing from his multicultural roots and his father’s pioneering HIV/AIDS research. An investigative documentary based on Luke’s journeys through seven African countries, diving into financial experiments and innovations—from mobile money and digital lending to Bitcoin—raising smart questions and offering potential lessons for the West. Its May appearance at BFF25 marks its largest European event to date, following festival screenings and nominations across multiple continents over the past year. HOTEL BITCOIN – A Spanish comedy directed by Manuel Sanabria and Carlos “Pocho” Villaverde. Four friends, 4,000 bitcoins , and one laptop spark a chaotic adventure of parties, love, crime, and a dash of madness. Exploring sound money, value, and relationships through a twisting plot. The film premiered at the Tarazona and Moncayo Comedy Film Festival in August 2024. Its Warsaw screening at BFF25 (in Spanish with English subtitles) marks its first public showing outside the Spanish-speaking world.Check out trailers for this year’s BFF25 and past editions on YouTube.

Tickets & Info:

- Detailed program and tickets are available at bitcoinfilmfest.com/bff25.

- Stay updated via the festival’s official channels (links provided on the website).

- Use ‘LN-NEWS’ to get 10% of tickets

-

@ b1ddb4d7:471244e7

2025-05-24 17:00:33

Starting January 1, 2026, the United Kingdom will impose some of the world’s most stringent reporting requirements on cryptocurrency firms.

All platforms operating in or serving UK customers-domestic and foreign alike-must collect and disclose extensive personal and transactional data for every user, including individuals, companies, trusts, and charities.

This regulatory drive marks the UK’s formal adoption of the OECD’s Crypto-Asset Reporting Framework (CARF), a global initiative designed to bring crypto oversight in line with traditional banking and to curb tax evasion in the rapidly expanding digital asset sector.

What Will Be Reported?

Crypto firms must gather and submit the following for each transaction:

- User’s full legal name, home address, and taxpayer identification number

- Detailed data on every trade or transfer: type of cryptocurrency, amount, and nature of the transaction

- Identifying information for corporate, trust, and charitable clients

The obligation extends to all digital asset activities, including crypto-to-crypto and crypto-to-fiat trades, and applies to both UK residents and non-residents using UK-based platforms. The first annual reports covering 2026 activity are due by May 31, 2027.

Enforcement and Penalties

Non-compliance will carry stiff financial penalties, with fines of up to £300 per user account for inaccurate or missing data-a potentially enormous liability for large exchanges. The UK government has urged crypto firms to begin collecting this information immediately to ensure operational readiness.

Regulatory Context and Market Impact

This move is part of a broader UK strategy to position itself as a global fintech hub while clamping down on fraud and illicit finance. UK Chancellor Rachel Reeves has championed these measures, stating, “Britain is open for business – but closed to fraud, abuse, and instability”. The regulatory expansion comes amid a surge in crypto adoption: the UK’s Financial Conduct Authority reported that 12% of UK adults owned crypto in 2024, up from just 4% in 2021.

Enormous Risks for Consumers: Lessons from the Coinbase Data Breach

While the new framework aims to enhance transparency and protect consumers, it also dramatically increases the volume of sensitive personal data held by crypto firms-raising the stakes for cybersecurity.

The risks are underscored by the recent high-profile breach at Coinbase, one of the world’s largest exchanges.

In May 2025, Coinbase disclosed that cybercriminals, aided by bribed offshore contractors, accessed and exfiltrated customer data including names, addresses, government IDs, and partial bank details.

The attackers then used this information for sophisticated phishing campaigns, successfully deceiving some customers into surrendering account credentials and funds.

“While private encryption keys remained secure, sufficient customer information was exposed to enable sophisticated phishing attacks by criminals posing as Coinbase personnel.”

Coinbase now faces up to $400 million in compensation costs and has pledged to reimburse affected users, but the incident highlights the systemic vulnerability created when large troves of personal data are centralized-even if passwords and private keys are not directly compromised. The breach also triggered a notable drop in Coinbase’s share price and prompted a $20 million bounty for information leading to the attackers’ capture.

The Bottom Line

The UK’s forthcoming crypto reporting regime represents a landmark in financial regulation, promising greater transparency and tax compliance. However, as the Coinbase episode demonstrates, the aggregation of sensitive user data at scale poses a significant cybersecurity risk.

As regulators push for more oversight, the challenge will be ensuring that consumer protection does not become a double-edged sword-exposing users to new threats even as it seeks to shield them from old ones.

-

@ b1ddb4d7:471244e7

2025-05-24 17:00:32

This article was originally published on aier.org

Even after eleven years experience, and a per Bitcoin price of nearly $20,000, the incredulous are still with us. I understand why. Bitcoin is not like other traditional financial assets.

Even describing it as an asset is misleading. It is not the same as a stock, as a payment system, or a money. It has features of all these but it is not identical to them.

What Bitcoin is depends on its use as a means of storing and porting value, which in turn rests of secure titles to ownership of a scarce good. Those without experience in the sector look at all of this and get frustrated that understanding why it is valuable is not so easy to grasp.

In this article, I’m updating an analysis I wrote six years ago. It still holds up. For those who don’t want to slog through the entire article, my thesis is that Bitcoin’s value obtains from its underlying technology, which is an open-source ledger that keeps track of ownership rights and permits the transfer of these rights. Bitcoin managed to bundle its unit of account with a payment system that lives on the ledger. That’s its innovation and why it obtained a value and that value continues to rise.

Consider the criticism offered by traditional gold advocates, who have, for decades, pushed the idea that sound money must be backed by something real, hard, and independently valuable. Bitcoin doesn’t qualify, right? Maybe it does.

Bitcoin first emerged as a possible competitor to national, government-managed money in 2009. Satoshi Nakamoto’s white paper was released October 31, 2008. The structure and language of this paper sent the message: This currency is for computer technicians, not economists nor political pundits. The paper’s circulation was limited; novices who read it were mystified.

But the lack of interest didn’t stop history from moving forward. Two months later, those who were paying attention saw the emergence of the “Genesis Block,” the first group of bitcoins generated through Nakamoto’s concept of a distributed ledger that lived on any computer node in the world that wanted to host it.

Here we are all these years later and a single bitcoin trades at $18,500. The currency is held and accepted by many thousands of institutions, both online and offline. Its payment system is very popular in poor countries without vast banking infrastructures but also in developed countries. And major institutions—including the Federal Reserve, the OECD, the World Bank, and major investment houses—are paying respectful attention and weaving blockchain technology into their operations.

Enthusiasts, who are found in every country, say that its exchange value will soar even more in the future because its supply is strictly limited and it provides a system vastly superior to government money. Bitcoin is transferred between individuals without a third party. It is relatively low-cost to exchange. It has a predictable supply. It is durable, fungible, and divisible: all crucial features of money. It creates a monetary system that doesn’t depend on trust and identity, much less on central banks and government. It is a new system for the digital age.

Hard lessons for hard money

To those educated in the “hard money” tradition, the whole idea has been a serious challenge. Speaking for myself, I had been reading about bitcoin for two years before I came anywhere close to understanding it. There was just something about the whole idea that bugged me. You can’t make money out of nothing, much less out of computer code. Why does it have value then? There must be something amiss. This is not how we expected money to be reformed.

There’s the problem: our expectations. We should have been paying closer attention to Ludwig von Mises’ theory of money’s origins—not to what we think he wrote, but to what he actually did write.

In 1912, Mises released The Theory of Money and Credit. It was a huge hit in Europe when it came out in German, and it was translated into English. While covering every aspect of money, his core contribution was in tracing the value and price of money—and not just money itself—to its origins. That is, he explained how money gets its price in terms of the goods and services it obtains. He later called this process the “regression theorem,” and as it turns out, bitcoin satisfies the conditions of the theorem.

Mises’ teacher, Carl Menger, demonstrated that money itself originates from the market—not from the State and not from social contract. It emerges gradually as monetary entrepreneurs seek out an ideal form of commodity for indirect exchange. Instead of merely bartering with each other, people acquire a good not to consume, but to trade. That good becomes money, the most marketable commodity.

But Mises added that the value of money traces backward in time to its value as a bartered commodity. Mises said that this is the only way money can have value.

The theory of the value of money as such can trace back the objective exchange value of money only to that point where it ceases to be the value of money and becomes merely the value of a commodity…. If in this way we continually go farther and farther back we must eventually arrive at a point where we no longer find any component in the objective exchange value of money that arises from valuations based on the function of money as a common medium of exchange; where the value of money is nothing other than the value of an object that is useful in some other way than as money…. Before it was usual to acquire goods in the market, not for personal consumption, but simply in order to exchange them again for the goods that were really wanted, each individual commodity was only accredited with that value given by the subjective valuations based on its direct utility.

Mises’ explanation solved a major problem that had long mystified economists. It is a narrative of conjectural history, and yet it makes perfect sense. Would salt have become money had it otherwise been completely useless? Would beaver pelts have obtained monetary value had they not been useful for clothing? Would silver or gold have had money value if they had no value as commodities first? The answer in all cases of monetary history is clearly no. The initial value of money, before it becomes widely traded as money, originates in its direct utility. It’s an explanation that is demonstrated through historical reconstruction. That’s Mises’ regression theorem.

Bitcoin’s Use Value

At first glance, bitcoin would seem to be an exception. You can’t use a bitcoin for anything other than money. It can’t be worn as jewelry. You can’t make a machine out of it. You can’t eat it or even decorate with it. Its value is only realized as a unit that facilitates indirect exchange. And yet, bitcoin already is money. It’s used every day. You can see the exchanges in real time. It’s not a myth. It’s the real deal.

It might seem like we have to choose. Is Mises wrong? Maybe we have to toss out his whole theory. Or maybe his point was purely historical and doesn’t apply in the future of a digital age. Or maybe his regression theorem is proof that bitcoin is just an empty mania with no staying power, because it can’t be reduced to its value as a useful commodity.

And yet, you don’t have to resort to complicated monetary theory in order to understand the sense of alarm surrounding bitcoin. Many people, as I did, just have a feeling of uneasiness about a money that has no basis in anything physical. Sure, you can print out a bitcoin on a piece of paper, but having a paper with a QR code or a public key is not enough to relieve that sense of unease.

How can we resolve this problem? In my own mind, I toyed with the issue for more than a year. It puzzled me. I wondered if Mises’ insight applied only in a pre-digital age. I followed the speculations online that the value of bitcoin would be zero but for the national currencies into which it is converted. Perhaps the demand for bitcoin overcame the demands of Mises’ scenario because of a desperate need for something other than the dollar.

As time passed—and I read the work of Konrad Graf, Peter Surda, and Daniel Krawisz—finally the resolution came. Bitcoin is both a payment system and a money. The payment system is the source of value, while the accounting unit merely expresses that value in terms of price. The unity of money and payment is its most unusual feature, and the one that most commentators have had trouble wrapping their heads around.

We are all used to thinking of currency as separate from payment systems. This thinking is a reflection of the technological limitations of history. There is the dollar and there are credit cards. There is the euro and there is PayPal. There is the yen and there are wire services. In each case, money transfer relies on third-party service providers. In order to use them, you need to establish what is called a “trust relationship” with them, which is to say that the institution arranging the deal has to believe that you are going to pay.

This wedge between money and payment has always been with us, except for the case of physical proximity.

If I give you a dollar for your pizza slice, there is no third party. But payment systems, third parties, and trust relationships become necessary once you leave geographic proximity. That’s when companies like Visa and institutions like banks become indispensable. They are the application that makes the monetary software do what you want it to do.

The hitch is that

-

@ b1ddb4d7:471244e7

2025-05-24 17:00:30

Breez, a leader in Lightning Network infrastructure, and Spark, a bitcoin-native Layer 2 (L2) platform, today announced a groundbreaking collaboration to empower developers with tools to seamlessly integrate self-custodial bitcoin payments into everyday applications.

The partnership introduces a new implementation of the Breez SDK built on Spark’s bitcoin-native infrastructure, accelerating the evolution of bitcoin from “digital gold” to a global, permissionless currency.

The Breez SDK is expanding

We’re joining forces with @buildonspark to release a new nodeless implementation of the Breez SDK — giving developers the tools they need to bring Bitcoin payments to everyday apps.

Bitcoin-Native

Powered by Spark’s…— Breez

(@Breez_Tech) May 22, 2025

(@Breez_Tech) May 22, 2025A Bitcoin-Native Leap for Developers

The updated Breez SDK leverages Spark’s L2 architecture to deliver a frictionless, bitcoin-native experience for developers.

Key features include:

- Universal Compatibility: Bindings for all major programming languages and frameworks.

- LNURL & Lightning Address Support: Streamlined integration for peer-to-peer transactions.

- Real-Time Interaction: Instant mobile notifications for payment confirmations.

- No External Reliance: Built directly on bitcoin via Spark, eliminating bridges or third-party consensus.

This implementation unlocks use cases such as streaming content payments, social app monetization, in-game currencies, cross-border remittances, and AI micro-settlements—all powered by Bitcoin’s decentralized network.

Quotes from Leadership

Roy Sheinfeld, CEO of Breez:

“Developers are critical to bringing bitcoin into daily life. By building the Breez SDK on Spark’s revolutionary architecture, we’re giving builders a bitcoin-native toolkit to strengthen Lightning as the universal language of bitcoin payments.”Kevin Hurley, Creator of Spark:

“This collaboration sets the standard for global peer-to-peer transactions. Fast, open, and embedded in everyday apps—this is bitcoin’s future. Together, we’re equipping developers to create next-generation payment experiences.”David Marcus, Co-Founder and CEO of Lightspark:

“We’re thrilled to see developers harness Spark’s potential. This partnership marks an exciting milestone for the ecosystem.”Collaboration Details

As part of the agreement, Breez will operate as a Spark Service Provider (SSP), joining Lightspark in facilitating payments and expanding Spark’s ecosystem. Technical specifications for the SDK will be released later this year, with the full implementation slated for launch in 2025.About Breez

Breez pioneers Lightning Network solutions, enabling developers to embed self-custodial bitcoin payments into apps. Its SDK powers seamless, secure, and decentralized financial interactions.About Spark

Spark is a bitcoin-native Layer 2 infrastructure designed for payments and settlement, allowing developers to build directly on Bitcoin’s base layer without compromises. -

@ bf47c19e:c3d2573b

2025-05-24 16:29:55

Originalni tekst na bitcoin-balkan.com.

Pregled sadržaja

- Šta je Bitcoin?

- Šta Bitcoin može da učini za vas?

- Zašto ljudi kupuju Bitcoin?

- Da li je vaš novac siguran u dolarima, kućama, akcijama ili zlatu?

- Šta je bolje za štednju od dolara, kuća i akcija?

- Po čemu se Bitcoin razlikuje od ostalih valuta?

- kako Bitcoin spašava svet?

- Kako mogu da saznam više o Bitcoin-u?

Bitcoin čini da štednja novca bude kul – i praktična – ponovo. Ovaj članak objašnjava kako i zašto.

Šta je Bitcoin?

Bitcoin se naziva digitalno zlato, mašina za istinu, blockchain, peer to peer mreža čvorova, energetski ponor i još mnogo toga. Bitcoin je, u stvari, sve ovo. Međutim, ova objašnjenja su često toliko tehnička i suvoparna, da bi većina ljudi radije gledala kako trava raste. Što je najvažnije, ova objašnjenja ne pokazuju kako Bitcoin ima bilo kakve koristi za vas.

iPod nije postao kulturološka senzacija jer ga je Apple nazvao „prenosnim digitalnim medijskim uređajem“. Postao je senzacija jer su ga zvali “1,000 pesama u vašem džepu.”

Ne zanima vas šta je Bitcoin. Vas zanima šta on može da učini za vas.

Baš kao i Internet, vaš auto, vaš telefon, kao i mnogi drugi uređaji i sistemi koje svakodnevno koristite, vi ne treba da znate šta je Bitcoin ili kako to funkcioniše da biste razumeli šta on može da učini za vas.

Šta Bitcoin može da učini za vas?

Bitcoin može da sačuva vaš teško zarađeni novac.

Bitcoin je stekao veliku pažnju u 2017. i 2018. godini zbog svoje spekulativne upotrebe. Mnogi ljudi su ga kupili nadajući se da će se obogatiti. Cena je naglo porasla, a zatim se srušila. Ovo nije bio prvi put da je Bitcoin uradio to. Međutim, niko nikada nije izgubio novac držeći bitcoin duže od 3,5 godine – ćak i ako je kupio na apsolutnim vrhovima.

Zašto Bitcoin konstantno raste? Ljudi počinju da shvataju koliko je Bitcoin moćan, kao način uštede novca u svetu u kojem je ’novac’ poput dolara, eura i drugih nacionalnih valuta dizajniran da gubi vrednost.

Ovo čini Bitcoin odličnom opcijom za štednju novca na nekoliko godina ili više. Bitcoin je bolji od štednje novca u dolarima, akcijama, nekretninama, pa čak i u zlatu.

Zato pokušajte da zaboravite na trenutak na razumevanje blockchaina, digitalne valute, kriptografije, seed fraza, novčanika, rudarstva i svih ostalih nerazumljivih termina. Za sada, razgovarajmo o tome zašto ljudi kupuju Bitcoin: razlog je prostiji nego što vi mislite.

Zašto ljudi kupuju Bitcoin?

Naravno, svako ima svoj razlog za kupovinu Bitcoin-a. Jedan od razloga, koji verovatno često čujete, je taj što mu vrednost raste. Ljudi žele da se obogate. Uskoče kao spekulanti, krenu u vožnju i najverovatnije ih prodaju ubrzo nakon kupovine.

Međutim, čak i kada cena krene naglo prema gore i strmoglavo padne nazad, mnogi ljudi ostanu i nakon tog pada. Otkud mi to znamo? Broj aktivnih novčanika dnevno, koji je otprilike sličan broju korisnika Bitcoin-a, nastavlja da raste. Takođe, nakon svakog balona u istoriji Bitcoin-a, cena se nikada ne vraća na svoju cenu pre balona. Uvek ostane malo višlja. Bitcoin se penje, a svaka masovna spekulativna serija dovodi sve više i više ljudi.

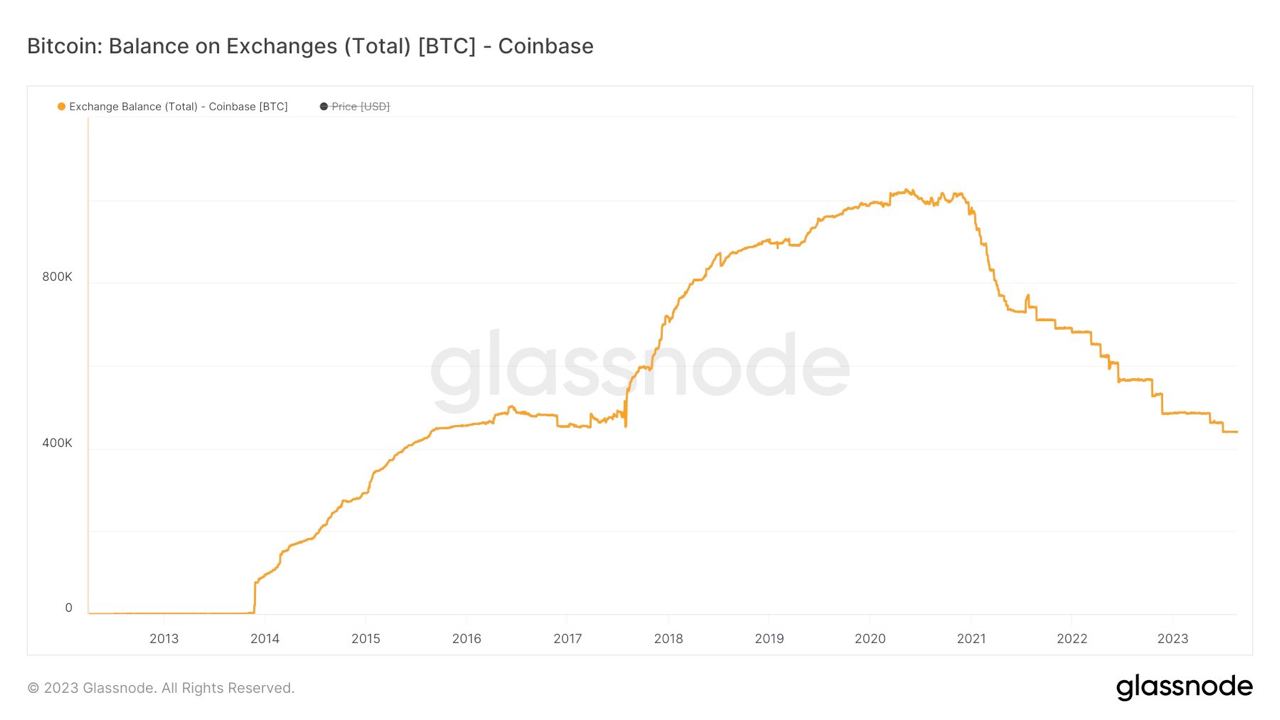

Broj aktivnih Bitcoin novčanika neprekidno raste

„Aktivna adresa“ znači da je neko tog dana poslao Bitcoin transakciju. Donji grafikon je na logaritamskoj skali.

Izvor: Glassnode

Izvor: GlassnodeCena Bitcoina se neprestano penje

Kroz istoriju Bitcoin-a možemo videti divlje kolebanje cena, ali nakon svakog balona, cena se ostaje višlja nego pre. Ovo je cena Bitcoin-a na logaritamskoj skali.

Izvor: Glassnode

Izvor: GlassnodeTo pokazuje da se ljudi zadržavaju: potražnja za Bitcoin-om se povećava. Da je svaki masovni rast cena bio samo balon koji su iscenirali prevaranti koji žele brzo da se obogate, cena bi se vratila na nivo pre balona. To se dogodilo sa lalama, ali ne i sa Bitcoin-om.

I zašto se onda cena Bitcoin-a stalno povećava? Sve veći broj ljudi čuva Bitcoin dugoročno – oni razumeju šta Bitcoin može učiniti za njihovu štednju.

Zašto ljudi štede svoj novac u Bitcoin-u umesto na štednim računima, kućama, deonicama ili zlatu? Hajde da pogledajmo sve te metode štednje, i zatim da ih uporedimo sa Bitcoin-om.

Da li je vaš novac siguran u dolarima, kućama, akcijama ili zlatu?

Tokom mnogo godina, to su bile pristojne opcije za štednju. Međutim, sistem koji podržava vrednost svega ovoga je u krizi.

Dolari, Euri, Dinari

Dolari i sve ostale „tradicionalne“ valute koje proizvode vlade, stvorene su da izgube vrednost kroz inflaciju. Banke i tradicionalni monetarni sistem uzrokuju inflaciju stalnim stvaranjem i distribucijom novog novca. Kada Američke Federalne Rezerve objave ciljanu stopu od 2% inflacije, to znači da žele da vaš novac svake godine izgubi 2% od svoje vrednosti. Čak i sa inflacijom od samo 2%, vaša štednja u dolarima izgubiće polovinu vrednosti tokom 40-godišnjeg radnog veka.

Izveštena inflacija se danas opasno povečava, uprkos rastućem „buretu sa barutom“ koji bi mogao da explodira i dovede do masivne hiperinflacije. Što je više valute u opticaju, to je više baruta u buretu.

Naše vlade su ekonomiju napunile valutama da bankarski sistem ne bi propao nakon finansijske krize koja se dogodila 2008. godine. Od tada je većina glavnih centralnih banaka postavila vrlo niske kamatne stope, što pojedincima i korporacijama omogućava dobijanje jeftinijih kredita. To znači da mnogi pojedinci i korporacije podižu ogromne kredite i koriste ih za kupovinu druge imovine poput deonica, umetničkih dela i nekretnina. Sve ovo pozajmljivanje znači da stvaramo tone novog novca i stavljamo ga u opticaj.

Računi za podsticaje (stimulus bills) COVID-19 za 2020. godinu unose trilione u sistem. Ovoliko stvaranje valuta na kraju dovodi do inflacije – velikog gubitka u vrednosti valute.

Količina američkog dolara u opticaju gotovo se udvostručila od marta 2020. godine. Izvor

Količina američkog dolara u opticaju gotovo se udvostručila od marta 2020. godine. IzvorRačuni za podsticaje su bez presedana, toliko da je neko izmislio meme da opiše ovu situaciju.

Resurs koji vlade mogu da naprave u većem broju da bi platile svoje račune? Ne zvuči kao dobro mesto za štednju novca.

Kuće

Kuće su tokom prošlog veka bile pristojan način štednje novca. Međutim, pad cena nekretnina 2007. godine doveo je do toga da su mnogi vlasnici kuća izgubili svu ušteđevinu.

Danas su kuće gotovo nepristupačne za prosečnog čoveka. Jedan od načina da se ovo izmeri je koliko godišnjih zarada treba prosečnom čoveku da zaradi ekvivalent vrednosti prosečne kuće. Prema CityLab-u, publikaciji Bloomberg-a koja pokriva gradove, porodica može da priuštiti određenu kuću ako košta manje od 2,6 godišnjih prihoda domaćinstva te porodice.

Međutim, prema RZS (Republički zavod za statistiku) prosečan prihod porodičnog domaćinstva u Srbiji iznosi oko 570 EUR mesečno ili otprilike 7.000 EUR godišnje. Nažalost, samo najjeftinija područja van gradova imaju srednje cene kuća od oko 2,6 prosečnih godišnjih prihoda domaćinstva. U većim gradovima poput Beograda i Novog Sada srednja cena kuće je veća od 10 prosečnih godišnjih prihoda jednog domaćinstva.

Ako nekako možete sebi da priuštite kuću, ona bi mogla biti pristojna zaliha vrednosti. Dokle god ne doživimo još jedan krah i izvršitelji zaplene ovu imovinu mnogim vlasnicima kuća.

Akcije

Berza je u prošlosti takođe dobro poslovala. Međutim, sporo i stabilno povećanje tržišta događa se u dosadnom, predvidljivom svetu. Svakog dana vidimo sve manje toga. Nakon ubrzanja korona virusa, videli smo smo najbrži pad američke berze u istoriji od 25% – brži od Velike depresije.

Neki se odlučuju za ulaganje u obveznice i drugu finansijsku imovinu, ali ’prinosi’ za tu imovinu – procenat kamate zarađene na imovinu iz godine u godinu – stalno opada. Sve veći broj odredjenih imovina ima čak i negativne prinose, što znači da posedovanje te imovine košta! Ovo je veliki problem za sve koji se oslanjaju na penziju. Plus, s obzirom na to da su akcije denominovane u tradicionalnim valutama poput dolara i evra, inflacija pojede prinos koji investitor dobije.

Najgore od svega je to što ti isti ekonomski krahovi koji uzrokuju masovna otpuštanja i teško tržište rada takođe znače i nagli pad cena akcija. Čuvanje ušteđevine u akcijama može značiti i gubitak štednje i gubitak posla zbog recesije. Teška vremena mogu da vas prisile da svoje akcije prodate po vrlo malim cenama samo da biste platili svoje račune.

A to nije baš siguran način štednje novca.

Zlato

Vrednost zlata neprekidno se povećavala tokom 5000 godina, obično padajući onda kada berza obećava jače prinose.

Evidencija vrednosti zlata je solidna. Međutim, zlato nosi i druge rizike. Većina ljudi poseduje zlato na papiru. Oni fizički ne poseduju zlato, već ga njihova banka čuva za njih. Zbog toga je zlato veoma podložno konfiskaciji od strane vlade.

Zašto bi vlada konfiskovala nečije zlato, a kamoli u demokratskoj zemlji u „slobodnom svetu“? Ali to se dešavalo i ranije. 1933. godine Izvršnom Naredbom 6102, predsednik Roosevelt naredio je svim Amerikancima da prodaju svoje zlato vladi u zamenu za papirne dolare. Vlada je iskoristila pretnju zatvorom za prikupljanje zlata u fizičkom obliku. Znali su da se zlato više poštuje kao zaliha vrednosti širom sveta od papirnih dolara.

Ako posedujete svoje zlato na nekoj od aplikacija za trgovanje akcijama, možete se kladiti da će vam ga država oduzeti ako joj zatreba. Čak i ako posedujete fizičko zlato, onda ga izlažete mogućnosti krađe – od strane kriminalca ili vaše vlade.

Vaša uštedjevina nije bezbedna.

Rast cena svih gore navedenih sredstava zavisi od našeg trenutnog političkog i ekonomskog sistema koji se nastavlja kao i tokom proteklih 100 godina. Međutim, danas vidimo ogromne pukotine u ovom sistemu.

Sistem ne funkcioniše dobro za većinu ljudi.

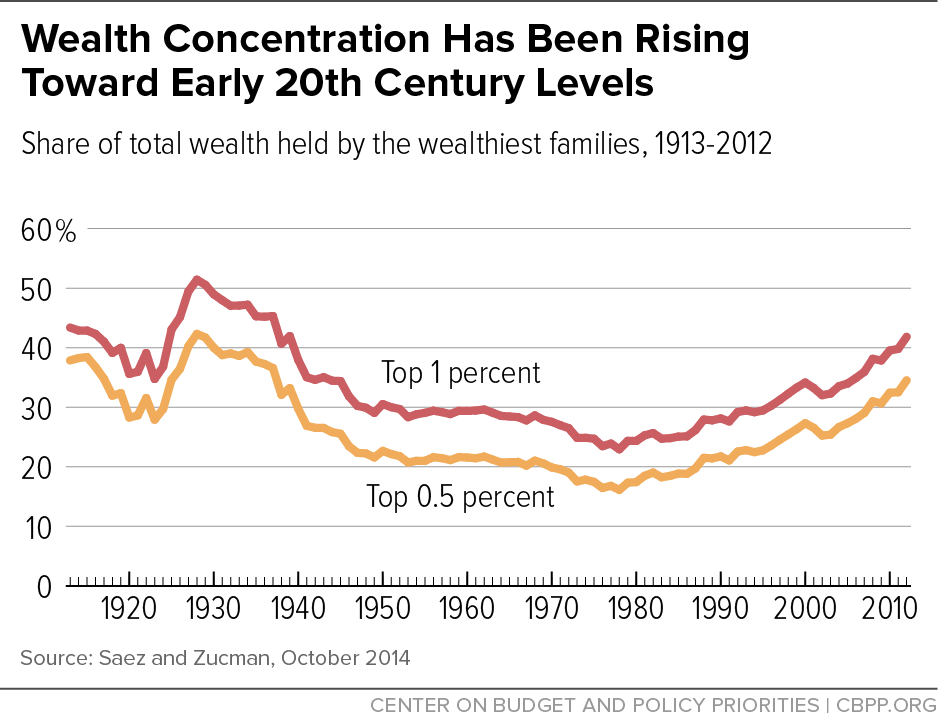

Od 1971. plate većine američkih radnika nisu rasle. S druge strane, bogatstvo koje imaju najbogatiji u društvu nalazi se na nivoima koji nisu viđeni više od 80 godina. U međuvremenu, ljudi sve manje i manje veruju institucijama poput banaka i vlada.

CBPP Nejednakost Bogatstva Tokom Vremena

CBPP Nejednakost Bogatstva Tokom VremenaŠirom sveta možemo videti dokaze o slamanju sistema kroz politički ekstremizam: izbor Trampa i drugih ekstremističkih desničarskih kandidata, Bregzit, pokret Occupy, popularizacija koncepta univerzalnog osnovnog dohotka, povratak pojma „socijalizam“ nazad u modu. Ljudi na svim delovima političkog i društvenog spektra osećaju problematična vremena i posežu za sve radikalnijim rešenjima.

Šta je bolje za štednju od dolara, kuća i akcija?

Pa kako ljudi mogu da štede novac u ovim teškim vremenima? Ili ne koriste tradicionalne valute, ili kupuju sredstva koja će zadržati vrednost u teškim vremenima.

Bitcoin ima najviše potencijala da zadrži vrednost kroz politička i ekonomska previranja od bilo koje druge imovine. Na tom putu će biti rupa na kojima će se rušiti ili pumpati, međutim, njegova svojstva čine ga takvim da će verovatno preživeti previranja kada druga imovina ne bude to mogla.

Šta Bitcoin čini drugačijim?

Bitcoini su retki.

Proces ‘rudarenja’ bitcoin-a, proizvodnju bitcoin-a čini veoma skupom, a Bitcoin protokol ograničava ukupan broj bitcoin-a na 21 milion novčića. To čini Bitcoin imunim na nagle poraste ponude. Ovo se veoma razlikuje od tradicionalnih valuta, koje vlade mogu da štampaju sve više kad god one to požele. Zapamtite, povećanje ponude vrši veliki pritisak na vrednost valute.

Bitcoini nemaju drugu ugovornu stranu.

Bitcoin se takođe razlikuje od imovine kao što su obveznice, akcije i kuće, jer mu nedostaje druga ugovorna strana. Druge ugovorne strane su drugi subjekti uključeni u vrednost sredstva, koji to sredstvo mogu obezvrediti ili vam ga uzeti. Ako imate hipoteku na svojoj kući, banka je druga ugovorna strana. Kada sledeći put dođe do velikog finansijskog kraha, banka vam može oduzeti kuću. Kompanije su kvazi-ugovorne strane akcijama i obveznicama, jer mogu da počnu da donose loše odluke koje utiču na njihovu cenu akcija ili na „neizvršenje“ duga (da ga ne vraćaju vama ili drugim poveriocima). Bitcoin nema ovih problema.

Bitcoin je pristupačan.

Svako sa 5 eura i mobilnim telefonom može da kupi i poseduje mali deo bitcoin-a. Važno je da znate da ne morate da kupite ceo bitcoin. Bitcoin-i su deljivi do 100-milionite jedinice, tako da možete da kupite Bitcoin u vrednosti od samo nekoliko eura. Neuporedivo lakše nego kupovina kuće, zlata ili akcija!

Bitcoin se ne može konfiskovati.

Banke drže većinu vaših eura, zlata i akcija za vas. Većina ljudi u razvijenom svetu veruje bankama, jer većina ljudi koji žive u današnje vreme nikada nije doživela konfiskaciju imovine ili ’šišanje’ od strane banaka ili vlada. Nažalost, postoji presedan za konfiskaciju imovine čak i u demokratskim zemljama sa snažnom vladavinom prava.

Kada vlada konfiskuje imovinu, ona obično ubedi javnost da će je menjati za imovinu jednake vrednosti. U SAD-u 1930-ih, vlada je davala dolare vlasnicima zlata. Vlada je znala da uvek može da odštampa još više dolara, ali da ne može da napravi više zlata. Na Kipru 2012. godine, jedna propala banka je svojim klijentima dala deonice banke da pokrije dolare klijenata koje je banka trebala da ima. I dolari i deonice su strmoglavo opali u odnosu na imovinu koja je uzeta od ovih ljudi.

Doći do bitcoin-a koji ljudi poseduju, biće mnogo teže jer se bitcoin-i mogu čuvati u novčaniku koji ne poseduje neka treća strana, a vi možete čak i da zapamtite privatne ključeve do vašeg bitcoin-a u glavi.

Bitcoin je za štednju.

Bitcoin se polako pokazuje kao najbolja opcija za dugoročnu štednju novca, posebno s obzirom na današnju ekonomsku klimu. Posedovanje čak i malog dela, je polisa osiguranja koja se isplati ako svet i dalje nastavi da ludi. Cena Bitcoin-a u dolarima može divlje da varira u roku od godinu ili dve, ali tokom 3+ godine skoro svi vide slične ili više cene od trenutka kada su ga kupili. U stvari, doslovno niko nije izgubio novac čuvajući Bitcoin duže od 3,5 godine – čak i ako je kupio BTC na apsolutnim vrhovima tržišta.

Imajte na umu da nakon ove tačke ti ljudi više nikada nisu videli rizik od gubitka. Cena se nikada nije smanjila niže od najviše cene u prethodnom ciklusu.

Po čemu se Bitcoin razlikuje od ostalih valuta?

Bitcoin funkcioniše tako dobro kao način štednje zbog svog neobičnog dizajna, koji ga čini drugačijim od bilo kog drugog oblika novca koji je postojao pre njega. Bitcoin je digitalna valuta, prvi i verovatno jedini primer valute koja ima ograničenu ponudu dok radi na otvorenom, decentralizovanom sistemu. Vlade strogo kontrolišu valute koje danas koristimo, poput dolara i eura, i proizvode ih za finansiranje ratova i dugova. Korisnici Bitcoin-a – poput vas – kontrolišu Bitcoin protokol.

Evo šta Bitcoin razlikuje od dolara, eura i drugih valuta:

Bitcoin je otvoren sistem.

Svako može da odluči da se pridruži Bitcoin mreži i primeni pravila softverskog protokola, što je dovelo do vrlo decentralizovanog sistema u kojem nijedan pojedinac ili entitet ne može da blokira transakciju, zamrzne sredstva ili da ukrade od druge osobe.Današnji savremeni bankarski sistem se uveliko razlikuje. Nekoliko banaka je dobilo poverenje da gotovo sve valute, akcije i druge vredne predmete čuvaju na “sigurnom” za svoje klijente. Da biste postali banka, potrebni su vam milioni dolara i neverovatne količine političkog uticaja. Da biste pokrenuli Bitcoin čvor i postali „svoja banka“, potrebno vam je nekoliko stotina dolara i jedno slobodno popodne.

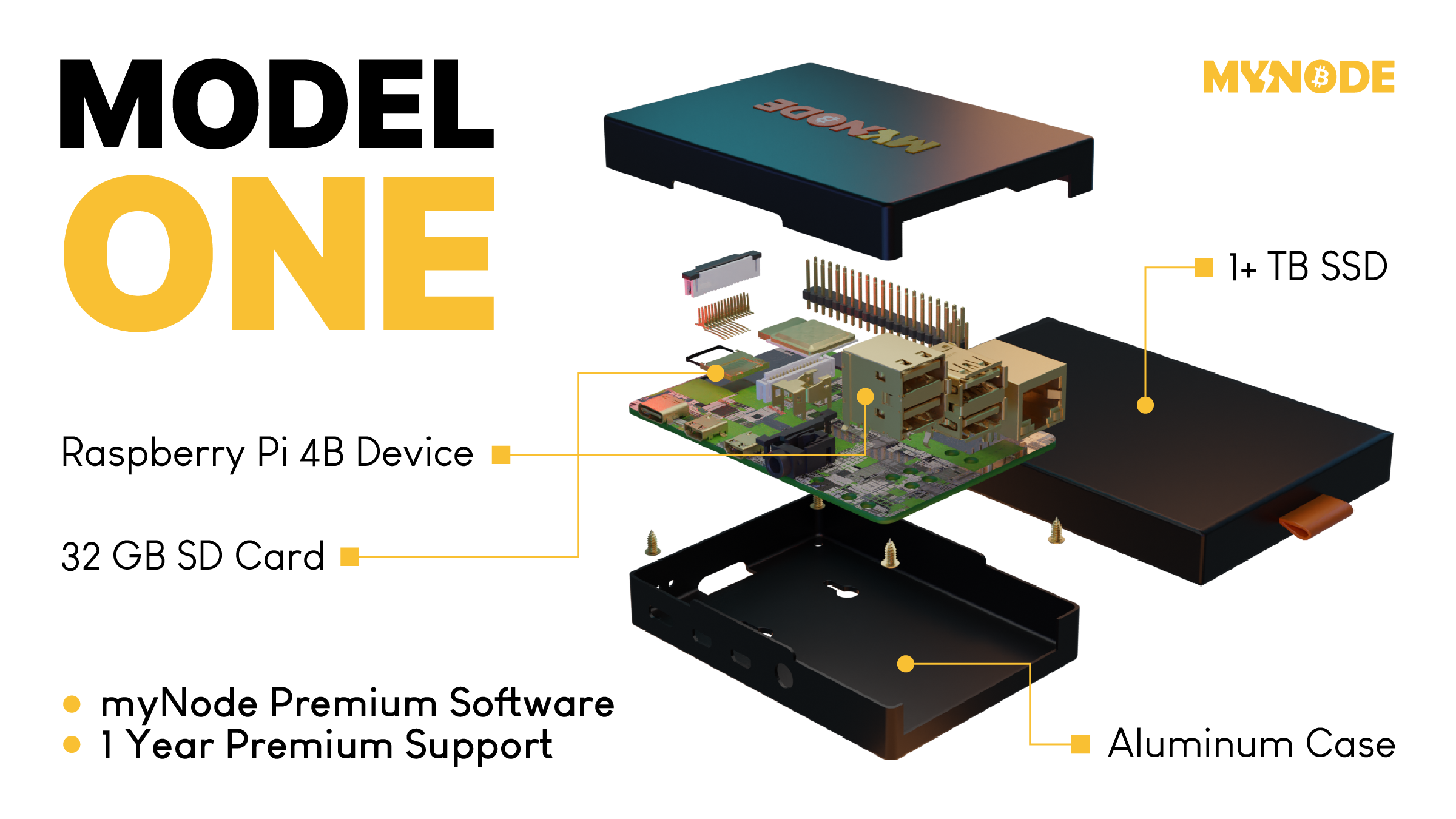

Tako izgleda Bitcoin čvor – Node

MyNode čvor vam omogućava da postanete svoja banka za samo nekoliko minuta.

Tako izgleda Bitcoin čvor – Node

MyNode čvor vam omogućava da postanete svoja banka za samo nekoliko minuta.Bitcoin ima ograničenu ponudu.

Softverski protokol otvorenog koda koji upravlja Bitcoin sistemom ograničava broj novih bitcoin-a koji se mogu stvoriti tokom vremena, sa ograničenjem od ukupno 21.000.000 bitcoin-a. S druge strane, valute koje danas koristimo imaju neograničenu ponudu. Istorija i sadašnje odluke centralnih banaka govore nam da će vlade uvek štampati sve više i više valuta, sve dok valuta ne bude bezvredna. Sve ovo štampanje uzrokuje inflaciju, što pravi štetu običnim radnim ljudima i štedišama.

Tradicionalne valute su dizajnirane tako da opadaju vremenom. Svaki put kada centralna banka kaže da cilja određenu stopu inflacije, oni ustvari kažu da žele da vaš novac svake godine izgubi određeni procenat svoje vrednosti.

Bitcoin-ova ograničena ponuda znači da je on tako dizajniran da raste vremenom kako se potražnja za njim povećava.

Bitcoin putuje oko sveta za nekoliko minuta.

Svako može da pošalje bitcoin-e za nekoliko minuta širom sveta, bez obzira na granice, banke i vlade. Potrebno je manje od minuta da se transakcija pojavi na novčaniku primaoca i oko 60 minuta da se transakcija u potpunosti „obračuna“, tako da primaoc može da bude siguran da su primljeni bitcoin-i sada njegovi (6 konfirmacija bloka). Slanje drugih valuta širom sveta traje danima ili čak mesecima ako se šalju milionski iznosi, a podrazumeva i visoke naknade.

Neke vlade i novinari tvrde da ova sloboda putovanja koju pruža Bitcoin pomaže kriminalcima i teroristima. Međutim, transakciju Bitcoin-a je lakše pratiti nego većinu transakcija u dolarima ili eurima.

Bitcoin se može čuvati na “USB-u”.

Dizajn Bitcoin-a je takav da vam treba samo da čuvate privatni ključ do svojih ‘bitcoin’ adresa (poput lozinke do bankovnih računa) da biste pristupili svojim bitcoin-ima odakle god poželite. Ovaj privatni ključ možete da sačuvate na disku ili na papiru u obliku 12 ili 24 reči na engleskom jeziku. Kao rezultat toga, možete da držite Bitcoin-e vredne milione dolara u svojoj šaci.

Sve ostale valute danas možete ili da strpate u svoj dušek ili da ih poverite banci na čuvanje. Za većinu ljudi koji žive u razvijenom svetu, i koji ne osporavaju autoritet i poverenje u banku, ovo deluje sasvim dobro. Međutim, oni kojima je potrebno da pobegnu od ugnjetavačke vlade ili koji naljute pogrešne ljude, ne mogu verovati bankama. Za njih je sposobnost da nose svoju ušteđevinu bez potrebe za ogromnim koferom neprocenjiva. Čak i ako ne živite na mestu poput ovog, cena Bitcoin-a se i dalje povećava kada ih neko kome oni trebaju kupi.

Kako Bitcoin spašava svet?

Bitcoin, kao ultimativni način štednje, je cakum pakum, ali da li on pomaže u poboljšanju sveta u celini?

Kao što ćete početi da shvatate, ulazeći sve dublje i u druge sadržaje na ovoj stranici, mnogi temeljni delovi našeg današnjeg monetarnog sistema i ekonomije su duboko slomljeni. Međutim, oni koji upravljaju imaju korist od ovakvih sistema, pa se on verovatno neće promeniti bez revolucije ili mirnog svrgavanja od strane naroda. Bitcoin predstavlja novi sistem, sa nekoliko glavnih prednosti:

- Bitcoin popravlja novac, koji je milenijumima služio kao važan alat za rast i poboljšanje društva.