-

@ bc6ccd13:f53098e4

2025-05-21 22:13:47

@ bc6ccd13:f53098e4

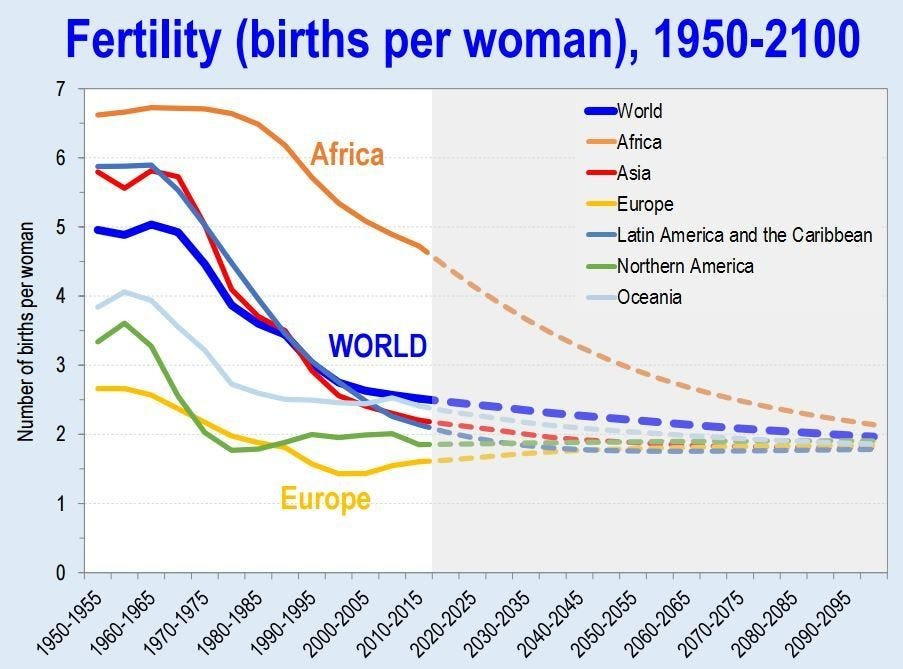

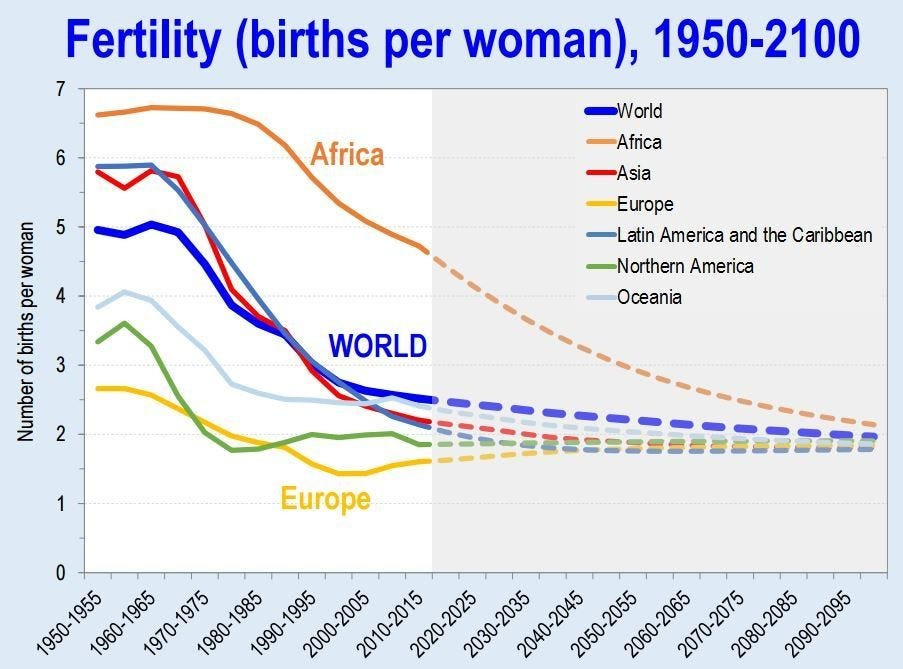

2025-05-21 22:13:47The global population has been rising rapidly for the past two centuries when compared to historical trends. Fifty years ago, that trend seemed set to continue, and there was a lot of concern around the issue of overpopulation. But if you haven’t been living under a rock, you’ll know that while the population is still rising, that trend now seems set to reverse this century, and there’s every indication population could decline precipitously over the next two centuries.

Demographics is a field where predictions about the future are much more reliable than in most scientific fields. That’s because future population trends are “baked in” decades in advance. If you want to know how many fifty-year-olds there will be in forty years, all you have to do is count the ten-year-olds today and allow for mortality rates. That maximum was already determined by the number of births ten years ago, and absolutely nothing can change that now. The average person doesn’t think that through when they look at population trends. You hear a lot of “oh we just need to do more of x to help the declining birthrate” without an acknowledgement that future populations in a given cohort are already fixed by the number of births that already occurred.

As you can see, global birthrates have already declined close to the 2.3 replacement level, with some regions ahead of others, but all on the same trajectory with no region moving against the trend. I’m not going to speculate on the reasons for this, or even whether it’s a good or bad thing. Instead I’m going to make some observations about outcomes this trend could cause economically, and why. Like most macro issues, an individual can’t do anything to change the global landscape personally, but knowing what that landscape might look like is essential to avoiding fallout from trends outside your control.

The Resource Pie

Thomas Malthus popularized the concern about overpopulation with his 1798 book An Essay on the Principle of Population. The basic premise of the book was that population could grow and consume all the available resources, leading to mass poverty, starvation, disease, and population collapse. We can say in hindsight that this was incorrect, given that the global population has increased from less than a billion to over eight billion since then, and the apocalypse Malthus predicted hasn’t materialized. Exactly the opposite, in fact. The global standard of living has risen to levels Malthus couldn’t have imagined, much less predicted.

So where did Malthus go wrong? His hypothesis seems reasonable enough, and we do see a similar trend in certain animal populations. The base assumption Malthus got wrong was to assume resources are a finite, limiting factor to the human population. That at some point certain resources would be totally consumed, and that would be it. He treated it like a pie with a lot of slices, but still a finite number, and assumed that if the population kept rising, eventually every slice would be consumed and there would be no pie left for future generations. That turns out to be completely wrong.

Of course, the earth is finite at some abstract level. The number of atoms could theoretically be counted and quantified. But on a practical level, do humans exhaust the earth’s resources? I’d point to an article from Yale Scientific titled Has the Earth Run out of any Natural Resources? To quote,

> However, despite what doomsday predictions may suggest, the Earth has not run out of any resources nor is it likely that it will run out of any in the near future. > > In fact, resources are becoming more abundant. Though this may seem puzzling, it does not mean that the actual quantity of resources in the Earth’s crust is increasing but rather that the amount available for our use is constantly growing due to technological innovations. According to the U.S. Geological Survey, the only resource we have exhausted is cryolite, a mineral used in pesticides and aluminum processing. However, that is not to say every bit of it has been mined away; rather, producing it synthetically is much more cost efficient than mining the existing reserves at its current value.

As it happens, we don’t run out of resources. Instead, we become better at finding, extracting, and efficiently utilizing resources, which means that in practical terms resources become more abundant, not less. In other words, the pie grows faster than we can eat it.

So is there any resource that actually limits human potential? I think there is, and history would suggest that resource is human ingenuity and effort. The more people are thinking about and working on a problem, the more solutions we find and build to solve it. That means not only does the pie grow faster than we can eat it, but the more people there are, the faster the pie grows. Of course that assumes everyone eating pie is also working to grow the pie, but that’s a separate issue for now.

Productivity and Division of Labor

Why does having more people lead to more productivity? A big part of it comes down to division of labor and specialization. The best way to get really good at something is to do more of it. In a small community, doing just one thing simply isn’t possible. Everyone has to be somewhat of a generalist in order to survive. But with a larger population, being a specialist becomes possible. In fact, that’s the purpose of money, as I explained here.

nostr:naddr1qvzqqqr4gupzp0rve5f6xtu56djkfkkg7ktr5rtfckpun95rgxaa7futy86npx8yqq247t2dvet9q4tsg4qng36lxe6kc4nftayyy89kua2

The more specialized an economy becomes, the more efficient it can be. There are big economies of scale in almost every task or process. So for example, if a single person tried to build a car from scratch, it would be extremely difficult and take a very long time. However, if you have a thousand people building a car, each doing a specific job, they can become very good at doing that specific job and do it much faster. And then you can move that process to a factory, and build machines to do specific jobs, and add even more efficiency.

But that only works if you’re building more than one car. It doesn’t make sense to build a huge factory full of specialized equipment that takes lots of time and effort to design and manufacture, and then only build one car. You need to sell thousands of cars, maybe even millions of cars, to pay off that initial investment. So division of labor and specialization relies on large populations in two different ways. First, you need a large population to have enough people to specialize in each task. But second and just as importantly, you need a large population of buyers for the finished product. You need a big market in order to make mass production economical.

Think of a computer or smartphone. It takes thousands of specialized processes, thousands of complex parts, and millions of people doing specialized jobs to extract the raw materials, process them, and assemble them into a piece of electronic hardware. And electronics are relatively expensive anyway. Imagine how impossible it would be to manufacture electronics economically, if the market demand wasn’t literally in the billions of units.

Stairs Up, Elevator Down

We’ve seen exponential increases in productivity over the past few centuries, resulting in higher living standards even as population exploded. Now, facing the prospect of a drastic trend reversal, what will happen to productivity and living standards? The typical sentiment seems to be “well, there are a lot of people already competing for resources, so if population does decline, that will just reduce the competition and leave a bigger slice of pie for each person, so we’ll all be getting wealthier as a result of population decline.”

This seems reasonable at first glance. Surely dividing the economic pie into fewer slices means a bigger slice for everyone, right? But remember, more specialization and division of labor is what made the pie as big as it is to begin with. And specialization depends on large populations for both the supply of specialized labor, and the demand for finished goods. Can complex supply chains and mass production withstand population reduction intact? I don’t think the answer is clear.

The idea that it will all be okay, and we’ll get wealthier as population falls, is based on some faulty assumptions. It assumes that wealth is basically some fixed inventory of “things” that exist, and it’s all a matter of distribution. That’s typical Marxist thinking, similar to the reasoning behind “tax the rich” and other utopian wealth transfer schemes.

The reality is, wealth is a dynamic concept with strong network effects. For example, a grocery store in a large city can be a valuable asset with a large potential income stream. The same store in a small village with a declining population can be an unprofitable and effectively worthless liability.

Even something as permanent as a house is very susceptible to network effects. If you currently live in an area where housing is scarce and expensive, you might think a declining population would be the perfect solution to high housing costs. However, if you look at a place that’s already facing the beginnings of a population decline, you’ll see it’s not actually that simple. Japan, for example, is already facing an aging and declining population. And sure enough, you can get a house in Japan for free, or basically free. Sounds amazing, right? Not really.

If you check out the reason houses are given away in Japan, you’ll find a depressing reality. Most of the free houses are in rural areas or villages where the population is declining, often to the point that the village becomes uninhabited and abandoned. It’s so bad that in 2018, 13.6% of houses in Japan were vacant. Why do villages become uninhabited? Well, it turns out that a certain population level is necessary to support the services and businesses people need. When the population falls too low, specialized businesses can no longer operated profitably. It’s the exact issue we discussed with division of labor and the need for a high population to provide a market for the specialist to survive. As the local stores, entertainment venues, and businesses close, and skilled tradesmen move away to larger population centers with more customers, living in the village becomes difficult and depressing, if not impossible. So at a certain critical level, a village that’s too isolated will reach a tipping point where everyone leaves as fast as possible. And it turns out that an abandoned house in a remote village or rural area without any nearby services and businesses is worth… nothing. Nobody wants to live there, nobody wants to spend the money to maintain the house, nobody wants to pay the taxes needed to maintain the utilities the town relied on. So they try to give the houses away to anyone who agrees to live there, often without much success.

So on a local level, population might rise gradually over time, but when that process reverses and population declines to a certain level, it can collapse rather quickly from there.

I expect the same incentives to play out on a larger scale as well. Complex supply chains and extreme specialization lead to massive productivity. But there’s also a downside, which is the fragility of the system. Specialization might mean one shop can make all the widgets needed for a specific application, for the whole globe. That’s great while it lasts, but what happens when the owner of that shop retires with his lifetime of knowledge and experience? Will there be someone equally capable ready to fill his shoes? Hopefully… But spread that problem out across the global economy, and cracks start to appear. A specialized part is unavailable. So a machine that relies on that part breaks down and can’t be repaired. So a new machine needs to be built, which is a big expense that drives up costs and prices. And with a falling population, demand goes down. Now businesses are spending more to make fewer items, so they have to raise prices to stay profitable. Now fewer people can afford the item, so demand falls even further. Eventually the business is forced to close, and other industries that relied on the items they produced are crippled. Things become more expensive, or unavailable at any price. Living standards fall. What was a stairway up becomes an elevator down.

Hope, From the Parasite Class?

All that being said, I’m not completely pessimistic about the future. I think the potential for an acceptable outcome exists.

I see two broad groups of people in the economy; producers, and parasites. One thing the increasing productivity has done is made it easier than ever to survive. Food is plentiful globally, the only issues are with distribution. Medical advances save countless lives. Everything is more abundant than ever before. All that has led to a very “soft” economic reality. There’s a lot of non-essential production, which means a lot of wealth can be redistributed to people who contribute nothing, and if it’s done carefully, most people won’t even notice. And that is exactly what has happened, in spades.

There are welfare programs of every type and description, and handouts to people for every reason imaginable. It’s never been easier to survive without lifting a finger. So millions of able-bodied men choose to do just that.

Besides the voluntarily idle, the economy is full of “bullshit jobs.” Shoutout to David Graeber’s book with that title. (It’s an excellent book and one I would highly recommend, even though the author was a Marxist and his conclusions are completely wrong.) A 2015 British poll asked people, “Does your job make a meaningful contribution to the world?” Only 50% said yes, while 37% said no and 13% were uncertain.

This won’t be a surprise to anyone who’s operated a business, or even worked in the private sector in general. There are three types of jobs; jobs that accomplish something productive, jobs that accomplish nothing of value, and jobs that actually hinder people trying to accomplish something productive. The number of jobs in the last two categories has grown massively over the years. This would include a lot of unnecessary administrative jobs, burdensome regulatory jobs, useless DEI and HR jobs, a large percentage of public sector jobs, most of the military-industrial complex, and the list is endless. All these jobs accomplish nothing worthwhile at best, and actively discourage those who are trying to accomplish something at worst.

Even among jobs that do accomplish some useful purpose, the amount of time spent actually doing the job continues to decline. According to a 2016 poll, American office workers spent only 39% of their workday actually doing their primary task. The other 61% was largely wasted on unproductive administrative tasks and meetings, answering emails, and just simply wasting time.

I could go on, but the point is, there’s a lot of slack in the economy. We’ve become so productive that the number of people actually doing the work to keep everyone fed, clothed, and cared for is only a small percentage of the population. In one sense, that’s a cause for optimism. The population could decline a lot, and we’d still have enough bodies to man the economic engine, as it were.

Aging

The thing with population decline, though, is nobody gets to choose who goes first. Not unless you’re a psychopathic dictator. So populations get old, then they get small. This means that the number of dependents in the economy rises naturally. Once people retire, they still need someone to grow the food, keep the lights on, and provide the medical care. And it doesn’t matter how much money the retirees have saved, either. Money is just a claim on wealth. The goods and services actually have to be provided by someone, and if that someone was never born, all the money in the world won’t change anything.

And the aging occurs on top of all the people already taking from the economy without contributing anything of value. So that seems like a big problem.

Currently, wealth redistribution happens through a combination of direct taxes, indirect taxation through deficit spending, and the whole gamut of games that happen when banks create credit/debt money by making loans. In a lot of cases, it’s very indirect and difficult to pin down. For example, someone has a “job” in a government office, enforcing pointless regulations that actually hinder someone in the private sector from producing something useful. Their paycheck comes from the government, so a combination of taxes on productive people, and deficit spending, which is also a tax on productive people. But they “have a job,” so who’s going to question their contribution to society? On the other hand, it could be a banker or hedge fund manager. They might be pulling in a massive salary, but at the core all they’re really doing is finding creative financial ways to transfer wealth from productive people to themselves, without contributing anything of value.

You’ll notice a common theme if you think about this problem deeply. Most of the wealth transfer that supports the unproductive, whether that’s welfare recipients, retirees, bureaucrats, corporate middle managers, or weapons manufacturers, is only possible through expanding the money supply. There’s a limit to how much direct taxation the productive will bear while the option to collect welfare exists. At a certain point, people conclude that working hard every day isn’t worth it, when taxes take so much of their wages that they could make almost as much without working at all. So the balance of what it takes to support the dependent class has to come indirectly, through new money creation.

As long as the declining population happens under the existing monetary system, the future looks bleak. There’s no limit to how much money creation and inflation the parasite class will use in an attempt to avoid work. They’ll continue to suck the productive class dry until the workers give up in disgust, and the currency collapses into hyperinflation. And you can’t run a complex economy without functional money, so productivity inevitably collapses with the currency.

The optimistic view is that we don’t have to continue supporting the failed credit/debt monetary system. It’s hurting productivity, messing up incentives, and contributing to increasing wealth inequality and lower living standards for the middle class. If we walk away from that system and adopt a hard money standard, the possibility of inflationary wealth redistribution vanishes. The welfare and warfare programs have to be slashed. The parasite class is forced to get busy, or starve. In that scenario, the declining population of workers can be offset by a massive shift away from “bullshit jobs” and into actual productive work.

While that might not be a permanent solution to declining population, it would at least give us time to find a real solution, without having our complex economy collapse and send our living standards back to the 17th century.

It’s a complex issue with many possible outcomes, but I think a close look at the effects of the monetary system on productivity shows one obvious problem that will make the situation worse than necessary. Moving to a better monetary system and creating incentives for productivity would do a lot to reduce the economic impacts of a declining population.

-

@ a19caaa8:88985eaf

2025-05-21 22:12:06

インターネット、だいすき!

-

@ bc6ccd13:f53098e4

2025-05-21 22:11:33

The Bitcoin price action since the US presidential election, and particularly today, November 11, has given me an excuse to revisit an idea I’ve written about before. I explained here that money doesn’t “flow into” assets, and that the terminology makes it difficult for people to understand how prices actually work.

nostr:naddr1qvzqqqr4gupzp0rve5f6xtu56djkfkkg7ktr5rtfckpun95rgxaa7futy86npx8yqqhy6mmwv4uj63r0v4ekutt594fx2ctvd3uj63nvdamj6jtww3hj6stw096xs6twvukkgmt9ws6xg86ht5t

The Bitcoin market this year has been a perfect illustration of the points I tried to make, which offers another angle to explain the concept.

Back in January, the first spot Bitcoin ETFs were launched for trading in the US market. This was heralded as a great thing for the Bitcoin price, and tracking “inflows” into these ETFs became a top priority for Bitcoin market analysts. The expectation of course was that more Bitcoin purchased by these ETFs would result in higher prices for the asset.

And sure enough, over the first two months of trading, from mid-January to mid-March, the combined “inflows” to the ETFs totaled around $11 billion. Over the same time frame, the Bitcoin price rose almost 60%, from around $43,000 to $68,000. As should be expected, right?

But then, over the next seven and a half months, from mid-March to early November, the ETFs saw another $11 billion in “inflows”. The Bitcoin price in mid-March? $68,000. In early November? All the way up to… $68,000. Seven and a half months of treading water.

So how can that be? How can $11 billion dollars flowing into an asset cause a 60% price rise once, and no price change at all the next time?

If you read my previous article linked above, you’ll see that the whole idea of money “flowing into” an asset is incorrect and misleading, and this is a perfect illustration why. If you step back a bit, you’ll see the folly of that mentality. So when the ETFs buy $11 billion dollars worth of Bitcoin, where does it come from? They obviously have to buy it from someone. As always, every transaction has a buyer and a seller. In this case, the sellers are current Bitcoin holders selling through OTC desks on the spot market.

So why focus on the ETF buying rather than the Bitcoin holder selling? Instead of saying there were $11 billion in inflows to the Bitcoin ETFs, why not say there were $11 billion in outflows from spot Bitcoin holders? It’s just as valid either way.

To take it a step further, many analysts were consistently confused all summer as Bitcoin ETFs continued to see “inflows” on days that the Bitcoin price stayed flat or even fell. So let’s imagine two consecutive days of $300 million daily “inflows” into the ETFs. The first day, the Bitcoin price rises 3%. The second day, the Bitcoin price falls 3%. The first day, headlines can read Bitcoin Price Rises 3% as ETFs See $300m in Inflows. The second day, headlines can read Bitcoin Price Falls 3% as Spot Bitcoin Holders See $300m in Outflows.

See the silliness of this whole idea? Money flows aren’t the cause of price movement. They’re a fake metric used as a post hoc justification for price moves by people who want you to believe they understand markets better than you.

Moving on to today, as I write this on the evening of November 11, Bitcoin is up 30% from $68,000 to $88,000 in the week since the November 5 election. It rose from $69,000 to $75,000 on election night alone, after US markets had closed and while there were no ETF “inflows” at all. In fact, the ETFs saw over a hundred million dollars in outflows on November 5, followed by an 8% single day price increase.

So if money flows don’t move price, what does?

Investor sentiment, that’s what.

Talking about money flows at all, as illustrated by the Bitcoin ETFs, requires arbitrarily dividing a single market into different segments to disguise the fact that every transaction has both a buyer and a seller, so every transaction has an equal dollar amount of “flows” in both directions. In actuality, price is set by a convergence between the highest price any potential buyer is willing to pay, and the lowest price any potential seller is willing to accept. And that number can change without a single transaction occurring, and without a single dollar “flowing” anywhere.

If every Bitcoin holder simultaneously decided tonight that the lowest price they’re willing to accept is $200,000 per Bitcoin, and a single potential buyer decided to buy a single dollar worth of Bitcoin at that price, that would be the new Bitcoin price tomorrow morning. No ETF “inflows” or institutional buying pressure or short squeezes or liquidations required, or any of the other excuses market analysts use to confuse normal people and make it seem like they have some deep esoteric insight into the workings of markets and future price action.

Don’t overcomplicate something as simple as price. If holders of an asset demand higher prices and potential buyers are willing to pay it, prices rise. If potential buyers of an asset offer lower prices and holders are willing to sell, prices fall. The constant interplay between all those individual investors sentiments is what forms a market and a price. The transferring of money between buyers and sellers is an effect of price, not a cause.

-

@ bc6ccd13:f53098e4

2025-05-21 22:03:04

Bullshit Jobs, for those unfamiliar, is the title of a 2018 book by anthropologist David Graeber. It’s well worth a read just for the fascinating research and the engaging writing style. The premise of the book is that many people work in jobs that contribute nothing to society, and would not be missed if they suddenly vanished overnight.

The data backs this up. In a 2015 British poll that asked “does your job make a meaningful contribution to the world?”, 37 percent of people said no, and another 13 percent weren’t sure. That’s fully half the population who can’t confidently say their job is even worth doing. And other polls have found similar or worse results.

The book was inspired by the overwhelming response to a 2013 article Graeber wrote titled On the Phenomenon of Bullshit Jobs: A Work Rant. The point I’d like to address is found here.

Over the course of the last century, the number of workers employed as domestic servants, in industry, and in the farm sector has collapsed dramatically. At the same time, ‘professional, managerial, clerical, sales, and service workers’ tripled, growing ‘from one-quarter to three-quarters of total employment.’ In other words, productive jobs have, just as predicted, been largely automated away (even if you count industrial workers globally, including the toiling masses in India and China, such workers are still not nearly so large a percentage of the world population as they used to be.)

But rather than allowing a massive reduction of working hours to free the world’s population to pursue their own projects, pleasures, visions, and ideas, we have seen the ballooning of not even so much of the ‘service’ sector as of the administrative sector, up to and including the creation of whole new industries like financial services or telemarketing, or the unprecedented expansion of sectors like corporate law, academic and health administration, human resources, and public relations.

These are what I propose to call ‘bullshit jobs’.

It’s as if someone were out there making up pointless jobs just for the sake of keeping us all working. And here, precisely, lies the mystery. In capitalism, this is precisely what is not supposed to happen. Sure, in the old inefficient socialist states like the Soviet Union, where employment was considered both a right and a sacred duty, the system made up as many jobs as they had to (this is why in Soviet department stores it took three clerks to sell a piece of meat). But, of course, this is the sort of very problem market competition is supposed to fix. According to economic theory, at least, the last thing a profit-seeking firm is going to do is shell out money to workers they don’t really need to employ. Still, somehow, it happens.

While corporations may engage in ruthless downsizing, the layoffs and speed-ups invariably fall on that class of people who are actually making, moving, fixing and maintaining things; through some strange alchemy no one can quite explain, the number of salaried paper-pushers ultimately seems to expand, and more and more employees find themselves, not unlike Soviet workers actually, working 40 or even 50 hour weeks on paper, but effectively working 15 hours just as Keynes predicted, since the rest of their time is spent organizing or attending motivational seminars, updating their facebook profiles or downloading TV box-sets.

The answer clearly isn’t economic: it’s moral and political.

In the book, Graeber expands on this idea with a very entertaining description of the many flavors of bullshit jobs, based on anecdotes from readers of his article. He follows that up with theories speculating on the cause of this situation. And wraps it all up with the conclusion that basically capitalists are all big meanies and invent bullshit jobs just to torture people and prevent the arrival of the Marxist utopia where no one has to do much real work and we all sit around and sing kumbaya and discuss philosophy. That’s too harsh a criticism of a very well researched and written book, but I have to confess I was sorely disappointed the first time I read it by the author’s failure to even entertain what seems like the obvious alternative explanation.

Graeber acknowledges in the book that it’s not surprising bullshit jobs exist inside government, although he doesn’t focus strongly enough on why that is. Like he does in the article, he tries to brush it off with the excuse that the same problem exists in the private sector. As he acknowledges, this isn’t supposed to happen in capitalism. He realizes that it makes no logical economic sense for a profit-seeking firm to hire workers to do nothing productive.

But then he follows that acknowledgement with the claim that “The answer clearly isn’t economic: it’s moral and political.” I’m sorry, what? How is that clear? How do you go from stating an obvious economic fact, to denying that the problem is economic, and call it “clear”.

“Still, somehow, it happens,” is not anywhere close to a sufficient explanation to rule out an economic factor.

The economic explanation

First, some definitions.

Capitalism is defined as “an economic system in which the means of production and distribution are privately or corporately owned and development occurs through the accumulation and reinvestment of profits gained in a free market.”

A free market is “an economic system in which prices are based on competition among private businesses and are not controlled or regulated by a government: a market operating by free competition.”

Now that we made sure we’re talking about the same thing, we can analyze this issue logically.

Capitalism and free markets work through competition for customers. It’s an economic law that a customer won’t pay more for the same good or service when they could pay less. Someone can try to make obscure and esoteric objections and force me to emphasize the word “same” and analyze what the good or service being purchased actually is, but everyone else understands this intuitively. So if two companies are offering the same product for sale, all things being equal, the company offering lower prices will attract the customers. Pretty simple stuff.

Of course, the goal for the company is to generate profits. It’s literally in the definition of the word “capitalism”. So any system in which companies have a goal other than generating profits is, by definition, not capitalism.

A company can increase its profits two ways: raising prices, or lowering costs. We don’t have to get too philosophical to realize that if a company is paying someone to do nothing, the company could increase profits by firing that person and lowering their costs of production.

So the question is, why don’t they? Why do they hire people who increase their costs and lower their profits, thereby making them less competitive? And more importantly, if they do make that mistake, why don’t their competitors undercut their prices and take all the customers and bankrupt them?

I don’t think we can dismiss the economic factor as off-handedly as Graeber does. After all, making a profit is the fundamental, definitional purpose of a business or company in a capitalist economy. To say “companies in this capitalist economy are doing something completely antithetical to the very principles and definition of capitalism, so obviously they’re not doing it for economic reasons” is something of a non sequitur.

The conclusion, to me, seems obvious. We don’t have a capitalist economy. As far as I can tell, that’s true by definition. If companies aren’t even trying to achieve the goal companies must achieve to survive in a capitalist economy, and somehow they’re still surviving, that’s proof of the non-capitalist nature of the economy.

Which part of the capitalist system are we missing?

Well, let’s start with the obvious: there’s a lot of government in our economy. The government isn’t privately owned, which makes it not capitalist by definition. So any part of the economy that’s government is not capitalist.

Why is government not capitalist? Because government is not motivated to provide goods and services at a profit. Why not? Because government does not sell goods and services into a free market. Government gives away goods and services to its “customers” for free, because they’re paid for by people other than the consumers of the service. That payment comes in one of two ways: taxes, and debt. It’s not a voluntary transaction.

Which part of the capitalist system might private companies be missing?

They could be lacking competition. That is, operating a monopoly or cartel. If there’s no competing business to provide goods at lower prices, the company could hire people for useless jobs and compensate by raising prices. This places them outside the definition of capitalism, since “free competition” is part of the definition of a free market. Monopolies and cartels often develop and survive through protection by the government, which emphasizes their un-capitalistic nature.

They could be in a temporary situation where the people making the management decisions are sufficiently insulated from the market forces at play that their poor decisions can persist for a while. Many companies begin to lose their competitive edge at some point, after getting big enough to have economic inertia and for the management to be less accountable for business performance. If a company has grown big enough, they can start making poor financial decisions and absorb the lost profits, sometimes for years, before losing their market share to a smaller, more competitive rival. This isn’t really an absence of capitalism, just the natural creative destruction necessary for capitalism to function. The problem comes when a company that’s obviously uncompetitive is prevented from failing through un-capitalistic means. Maybe they’re big enough and wealthy enough to pressure the government into granting them monopoly status. This doesn’t have to be open, it’s often through creating such an impenetrable legal morass around the industry that no competitor can emerge. Or it can be in the form of a “too big to fail” direct government bailout.

The company could also be lacking that essential link between customer satisfaction and business income. In other words, maybe they aren’t selling to their customers. That can happen for various reasons.

Some companies are “private companies” but sell to the government. The government is not a customer in the capitalist sense, because the government spends money taken coercively from its subjects, not money earned voluntarily in the free market. So any company like Raytheon or Boeing that survives off government contracts can’t be accurately called a capitalist organization.

In an industry like healthcare, where the insurance companies are the middlemen in basically all transactions between patients and doctors, there are also lots of ways for bullshit jobs to proliferate. Patients don’t care how much a procedure costs, just that it helps them. Doctors don’t care how much a procedure costs, just that the insurance company will pay for it. And insurance companies don’t care whether a procedure helps the patient, they just want to collect as many premiums as possible while paying out as little for care as possible. The fact that the patient isn’t paying the doctor for their care breaks the necessary link between customer and producer that’s essential for a free market to function. That combines with the regulatory moat and cartel-like structure of the healthcare industry to prevent the competitive function of capitalism from occurring.

Companies could also be surviving off of money from someone other than their customers: bankers and investors. There’s obviously a role in a capitalist system for investors to support a new venture until it’s able to attract customers and establish a stable and profitable business model. But many companies today exist for much longer than economically reasonable without turning a profit. In the US, almost 2,000 of the 5,000 publicly traded companies with data available were classified as “zombie companies”, meaning they don’t even make enough profit to pay the interest on their debt. So they’re going deeper in the hole every year. How can this continue?

Well, the alternative to paying off your debt, is to borrow even more money to make payments on the debt you already owe. If this sounds similar to how the US government survives, then you’re beginning to get the picture.

How can banks keep loaning money to unprofitable businesses? And why would they do it? It doesn’t make sense… until you understand how banking works.

That’s really the core focus of most of my writing, and I’ve written multiple articles on money and banking explaining how the system works as I understand it. This would be a good one focused on banking specifically.

nostr:naddr1qvzqqqr4gupzp0rve5f6xtu56djkfkkg7ktr5rtfckpun95rgxaa7futy86npx8yqqt4g6r994pxjeedgfsku6edf35k2tt5de4nvdtzhjwrp2

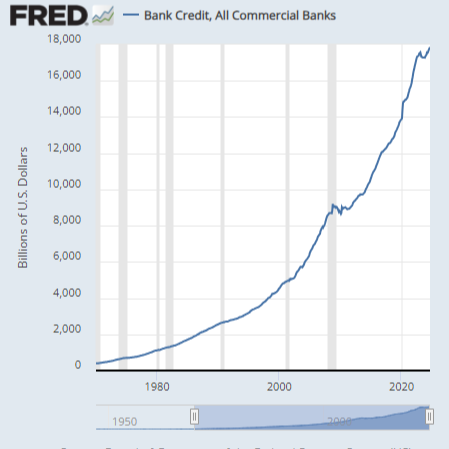

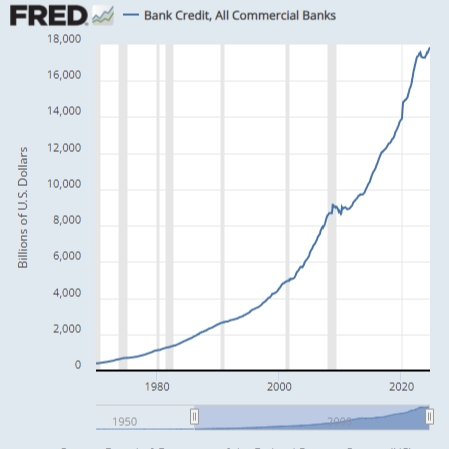

To very briefly recap, banks don’t make loans by taking in money from depositors and loaning that money to borrowers. Instead, banks create new money that never existed before out of thin air and loan that new money to borrowers. Banks make a profit by charging borrowers interest on this newly created money, which costs them nothing to create. A pretty cushy gig, if you can get it.

So from the perspective of the banks, the more loans and debt outstanding, the better. Every dollar of debt is a dollar they can collect interest on. It cost them nothing to create, so the more, the merrier. In fact, the banks would prefer that the loan principle never be repaid, because once it’s repaid, they can no longer collect interest on that loan until they make another loan to replace it. As long as the borrower keeps paying interest, the banks are happy. And if they need to lend the borrower some more money so he can afford to pay the interest, that’s fine too. Anything but letting the loan default.

Given those incentives, how do you expect a chart of the outstanding loans and credit of US commercial banks to look?

If you guessed up only, you’d be correct.

So what does this banking system have to do with bullshit jobs? Well, I’d argue that the fractionally reserved fiat banking system, in and of itself, is an anti-capitalist system. Money is the communication layer of capitalism, as I’ve previously written.

nostr:naddr1qvzqqqr4gupzp0rve5f6xtu56djkfkkg7ktr5rtfckpun95rgxaa7futy86npx8yqq247t2dvet9q4tsg4qng36lxe6kc4nftayyy89kua2

When one group of people can create money out of thin air, they have the ability to reallocate wealth in the economy. As long as the money is still functional, of course. Too much money creation and wealth reallocation, and people stop trusting the money. That’s when inflation becomes hyperinflation, the money no longer functions, and the whole system implodes.

Wealth reallocation by a small select group is the essence of a centrally planned socialist/Marxist economy. And we all know how efficient those economies are. In fact, Graeber himself mentioned the inefficiency of socialist states like the Soviet Union in his original article, and was not at all surprised by the existence of bullshit jobs in such an economic system. When wealth can be reallocated by central planners without regard to people’s preferences in a free market, inefficiency is never punished, so zombie companies full of bullshit jobs never go bankrupt.

The same thing happens under our “capitalist” system. Zombie companies full of bullshit jobs can get almost unlimited funding from too-big-to-fail banks, who don’t care whether they repay the loans, as long as they stay in business and keep making the interest payments. Sometimes the funding is in the form of loans directly, sometimes it’s in the form of massive stock market bubbles inflated by the endless money creation, sometimes through junk bond issuance funded by the same bubble economics, and sometimes it’s venture capital funds flush with liquidity for the same reason. Regardless, the cause, and the outcome, are the same.

The corrupt bankers own the corrupt politicians, so when the inevitable so-called black swan event occurs and the rotten edifice starts to quiver, another bailout is promptly rolled out. The government borrows trillions from their owners over at the Federal Reserve, who create the money out of thin air. The government sends it on over to the bankers who got caught with their hand in the cookie jar once again, and they paper over the massive holes in their balance sheet caused by blowing asset bubbles and funding inefficient zombie companies. Or sometimes, the government skips the middlemen entirely and bails out Boeing or whoever it happens to be directly.

And once again, bullshit jobs that couldn’t survive free market competition are rewarded at the expense of savers and taxpayers. As always, this flood of new liquidity flows out through the economy, causing inflation and boosting income for other inefficient companies that also deserved to fail. Creative destruction, a fundamental feature of a capitalist system, is avoided once again.

In my opinion, the banking system is at the root of the problem causing the proliferation of bullshit jobs. The system itself is, by design, fundamentally anti-capitalist in nature and function. It’s really a giant privately owned economic central planning system, in which a small fraction of people determine how resources are allocated, with privatized profits and socialized losses. The Soviet technocrats would be jealous.

Unfortunately, the bankers have successfully connected their industry so tightly to the term “capitalist” that showing people they’re anything but is almost impossible. To paraphrase the well-known quote, the greatest trick the bankers ever pulled was convincing the world that they’re the real capitalists.

Until the banking and monetary system fundamentally changes, inefficiency will persist and bullshit jobs will continue to proliferate. In my opinion, the problem is very much an economic problem. And it’s not a “late-stage capitalism” problem, it’s a “capitalism left the building a century ago” problem. We don’t need to get rid of capitalism, we’ve already done that. We need to bring sound money, and with it the possibility of a capitalist economy, back again.

-

@ 8bad92c3:ca714aa5

2025-05-21 22:01:27

Key Takeaways

In this episode of the TFTC podcast, Dom Bei—a firefighter, union leader, and CalPERS Board of Trustees candidate—makes a powerful case for why the largest pension fund in the U.S. must seriously consider Bitcoin as both an investment opportunity and an educational tool. Highlighting CalPERS’ missed decade in private equity and its troubling 75% funded status, Bei critiques the system’s misaligned incentives and high leadership turnover. He argues that Bitcoin offers more than just potential gains—it forces participants to confront foundational issues like inflation, wealth extraction, and financial literacy. Through his nonprofit Proof of Workforce, Bei has already helped unions adopt Bitcoin in self-custody and believes that small, incremental steps can drive reform. His campaign is about re-engaging the 2 million CalPERS members, challenging political inertia, and avoiding another decade of lost opportunity.

Best Quotes

"Bitcoin’s brand is resilience, and that cannot be undone."

"I don’t need to convince pensions to buy Bitcoin. I just need them to look into it."

"The first pension was funded with confiscated warships. The original incentive structure was theft."

"CalPERS is the second-largest purchaser of medical insurance in the U.S., behind the federal government."

"Only 10% of CalPERS members voted in the last board election. That’s insane."

"Bitcoin’s simplest features remain its most impressive: you hold something that’s yours, and no one can take it."

"We don’t need pensions to go all in. Just get off zero."

"Mainstream media has run an 80% negative campaign on Bitcoin for a decade. That’s not a conspiracy—it’s just math."

Conclusion

Dom Bei’s conversation with Marty Bent frames Bitcoin not as a cure-all, but as a critical tool worth exploring—one that promotes financial literacy, institutional accountability, and personal sovereignty. His call for education, transparency, and incremental reform challenges broken pension governance and urges workers to reclaim control over both their retirements and their understanding of money. In a landscape of growing liabilities and political interference, Bei’s campaign sparks a vital conversation at the intersection of sound money and public service—one that aligns closely with Bitcoin’s foundational ethos.

Timestamps

0:00 - Intro

0:32 - Opportunity Cost app

3:34 - Dom's background

10:36 - Fold & Bitkey

12:13 - How pensions got to this point

19:29 - Impact of failure

28:10 - Unchained

28:38 - CalPERS politicized

33:49 - How pensions should approach bitcoin

42:49 - How to educate

49:37 - Energy/mining

55:55 - Running for the board

1:08:52 - Roswell NM

1:12:33 - C2ATranscript

(00:00) pension funds are chasing liabilities and having to basically be these vehicles that play in the big kids sandbox. It's cutthroat and there's no mercy there. I can't imagine a world where the pension goes bust, that's going to send shock waves through so many different sectors of the economy. I mean, you're talking global impact.

(00:17) If you have a CIO that's incentivized for the fund to do well, they're going to find Bitcoin. The numbers don't lie. Bitcoin's brand is resilience, and that cannot be undone. What's up, freaks? Sitting down with Dom Bay, running for the board of trustees of Kalpers. Dom, welcome to the show. Thanks, Marty.

(00:44) And uh uh what else? What is up, freaks? How's everyone doing today? I hope everybody's doing well. Vibes are high here. Uh been vibe coding. The vibes are high because the vibe coding has been up. I vibe coded something last night. Feeling pretty excited. Nice. What were you working on? Is it a top secret or uh No, I think by the time this episode airs, I'll have released it, but it's a simple, very simple product.

(01:07) Uh, a browser extension that allows you to put the price of goods that you may or may not be buying in SATS alongside dollars so that you recognize the opportunity cost of purchasing things. Uh, I like that. That's that's you know I was working once with a hotel that was looking at doing Bitcoin like you know different Bitcoin stuff whether it's like putting on the treasury and one of the things I told him I was like you guys should just do a coffee shop where you just have dollar price and sats price just next to each

(01:38) other. It' be a cool thing you know something that we don't see a lot as Bitcoiners but just to you know we all do it. you get that familiarity where you go like, well, what would this be in SATS? And it's easy to look up big things but not little things. Um, so that's really cool, man. That's a that's a that'll be that'll be good. Yeah.

(01:56) The whole idea is to just have the concept of opportunity costs while you're spending front of mind, while you're shopping on the internet, which I think actually ties in perfectly with what we're here to talk about today with you specifically, is the opportunity costs that exist within pensions um that are deploying capital in ways that they have for many decades and many are missing.

(02:23) uh the Bitcoin boat. Many who haven't spoken to you are missing the Bitcoin boat and you are taking it upon yourself to try to tackle one of the biggest behemoths in the world of pensions and Kalpers to really drive home this opportunity cost at at the pension level. Yeah, for sure. you know, the outgoing chief investment officer of Kalpers, uh, Nicole Muso, uh, described the 10-year era of private equity that KPERS missed as the lost decade.

(02:56) Uh, it was the pinnacle of private equity, and Kalpers really felt like they didn't have enough capital uh, deployed. And you know, in past conversations, I've I've talked about, you know, knowing what we know about Bitcoin and where it's at and where it's going. Are you going to have similar commentary from pensions around the country in 2035 saying, "Hey, we're going to get into Bitcoin now.

(03:21) We we had a lost decade where it was just staring us right in the face and oh, we didn't really need to do much but learn about it and uh we missed the boat. So now, you know, let's let's learn about it. It'll be time will tell. Yeah. Let's jump into how you got to the point where you decided to run for the board of trustees at Kalpers.

(03:46) Let's get into your history uh as a firefighter working with the union and then your advocacy in recent years going out to public pensions, particularly those of emergency responders to to get Bitcoin within their their pension systems. and yeah, why you think Kalpers is the next big step for you? For sure. So, um I got hired as a firefighter uh just around I'm coming up on my 16-year anniversary.

(04:11) Uh I got hired as a firefighter in Santa Monica and early in my career as a firefighter. Uh someone reached out and said, "Hey, you know, you're you're you're kind of a goofball. You like talking to people and and um there's this person on the board who does a lot of our political stuff. he's leaving. You should get with him and kind of learn about what he does and go find out. And so, uh, I went with him.

(04:36) First thing he did was bring me to this breakfast with a city council member and we were talking history in the city and and I just like, you know, I love that kind of stuff and learning about, you know, the backstories behind whatever's going on and all the moving pieces. And so, uh, I ended up getting on our board, um, for the Santa Monica firefighters and pretty pretty young, doing a lot of the political stuff, ended up becoming the vice president and then became the president of the firefighters and what was over a 10-year period of serving as

(05:07) an elected board member for the firefighters. Um, you know, kind of parallel to that and unrelated, I found Bitcoin in 2017 uh randomly working at a conference, which um I forget which conference it was, but I kind of looked back and I think it might have been consensus. I'm not sure. Um, but this was 2017 and I remember my one takeaway from this conference which may or may not have been consensus and it was this.

(05:39) The people I spoke to there were equally or greater as uh convicted as any group or constituency I'd ever met in my entire life. That's including firefighters. Um you know like like any group the conviction was was was unmissable. Uh and you could tell the people I talked to there they would not be uh convinced otherwise.

(06:08) And uh at that time, you know, there wasn't as much of a division between the different coins, you know, like like there was Ethereum people there and there was Bitcoiners there, but there was a definite like someone got a hold of me and was like, "Hey, uh Bitcoin is something that like forget all this other stuff.

(06:25) You need to just learn this." And and I remember taking that away and kind of got passively involved. Wasn't super active in the space. um just kind of like you know learned about it and grabbed a little bit and and you know just kind of did that thing. the board took up a lot of my time. And so, um, another thing that happened while I was on the board was I was appointed to a pension advisory committee for the city of Santa Monica where we had a full presentation from the board uh, and um, they came and presented to us and and different um,

(06:58) not the board, it was like different team members. And so I learned a ton about the pension and and I've always been a I was a history major in college, so I love learning about history. and I started really getting into the history of pensions which is fascinating. We'll save that for another episode for the sake of your viewers.

(07:18) Um but but um started doing that and when I got off the board um you know in addition to this -

@ cae03c48:2a7d6671

2025-05-21 21:01:22

Bitcoin Magazine

U.S. Leads the World in Bitcoin Ownership, New Report ShowsA new report from River reveals that the United States dominates Bitcoin ownership globally, holding about 40% of all available Bitcoin. With 14.3% of its population owning Bitcoin, the U.S. outpaces Europe, Oceania, and Asia combined.

The United States is the global Bitcoin superpower.

Our new report breaks down how this advantage can fuel the next era of American prosperity. pic.twitter.com/v5BNgTGsKA

— River (@River) May 20, 2025

Corporate America also leads in Bitcoin holdings. Thirty-two U.S. public companies, with a combined market cap of $1.26 trillion, hold Bitcoin as a treasury asset. These firms account for 94.8% of all Bitcoin owned by publicly traded companies worldwide. Major holders include Strategy with 569,000 BTC, U.S. mining companies with 96,000 BTC, and others with 68,000 BTC, totaling 733,000 BTC in the U.S., compared to 40,000 BTC held elsewhere.

Since China’s ban on Bitcoin mining in 2021, the United States has become the global leader in Bitcoin mining, responsible for 38% of all new Bitcoin mined since then. The U.S. attracts miners thanks to its stable regulatory environment, access to deep and liquid capital markets, and abundant energy resources. These advantages have helped the U.S. increase its share of the global Bitcoin mining hashrate by over 500% since 2020, solidifying its position as the center of the industry.

Bitcoin is also emerging as America’s preferred reserve asset, overtaking gold. Over 49.6 million Americans are in favor of holding Bitcoin, compared to 36.7 million who still prefer gold.

The US government’s bitcoin advantage is greater than that of gold, where the US accounts for just 29.9% of the world’s central bank gold reserves.

“Because there is a fixed supply of BTC, there is a strategic advantage to being among the first nations to create a strategic bitcoin reserve,” said the White House on March 7, 2025.

Politically, support for Bitcoin is gaining significant momentum across the U.S. government. As of now, 59% of U.S. Senators and 66% of House Representatives openly support pro-Bitcoin policies, signaling a notable shift in political attitudes and greater acceptance of digital assets as key components of America’s economic future.

The study highlights that Bitcoin ownership is highest among American males aged 31-35 and 41-45, with ownership rates ranging from 3% to 41% within these age groups. Politically, those identifying as “very liberal” or “neutral” are more likely to own Bitcoin than conservatives, though conservatives still make up a significant portion of holders.

This post U.S. Leads the World in Bitcoin Ownership, New Report Shows first appeared on Bitcoin Magazine and is written by Oscar Zarraga Perez.

-

@ cae03c48:2a7d6671

2025-05-21 21:01:21

Bitcoin Magazine

The Blockchain Group Secures €8.6 Million to Boost Bitcoin StrategyThe Blockchain Group (ALTBG), listed on Euronext Growth Paris and known as Europe’s first Bitcoin Treasury Company, has announced a capital increase of approximately €8.6 million as it pushes forward with its Bitcoin Treasury Company strategy. The funding was raised through two operations, a Reserved Capital Increase and a Private Placement, with both priced at €1.279 per share.

JUST IN:

French company The Blockchain Group raises €8.6 million to buy more #Bitcoin pic.twitter.com/VjTKyFSS6w

French company The Blockchain Group raises €8.6 million to buy more #Bitcoin pic.twitter.com/VjTKyFSS6w— Bitcoin Magazine (@BitcoinMagazine) May 20, 2025

This price represents a 20.18% premium over the 20-day volume-weighted average share price but a 46.26% discount compared to the closing price on May 19, 2025, reflecting recent high share price volatility.

“The Company’s Board of Directors decided on May 19, 2025, using the delegated authority granted by the shareholders’ meeting held on February 21, 2025, under the terms of its 5th resolution, on an issuance, without pre-emptive rights for shareholders, of 3,368,258 new ordinary shares of the Company at a price of €1.2790 per share, including an issuance premium, representing a premium of approximately 20.18% compared to the weighted average of the twenty closing prices of ALTBG shares on Euronext Growth Paris preceding the decision of the Company’s Board of Directors, corresponding to a total subscription amount of €4,308,001.98,” said the press release.

In the Reserved Capital Increase, 3.37 million shares were issued to selected investors, including Robbie van den Oetelaar, TOBAM Bitcoin Treasury Opportunities Fund, and Quadrille Capital, raising over €4.3 million. The Private Placement raised another €4.35 million via the issuance of 3.4 million shares, targeting qualified investors.

“The Board of Directors also decided on a capital increase without pre-emptive rights for shareholders through an offering exclusively targeting a limited circle of investors acting on their own behalf or qualified investor, ” stated the press release.

The funds will support The Blockchain Group’s ongoing strategy of accumulating Bitcoin and expanding its subsidiaries in data intelligence, AI, and decentralized tech. Following this capital increase, the company’s share capital stands at €4.37 million, divided into over 109 million shares.

“The funds raised through the Capital Increase will enable the Company to strengthen its Bitcoin Treasury Company strategy, consisting in the accumulation of Bitcoin, while continuing to develop the operational activities of its subsidiaries,” said the press release.

Additionally, on May 12, The Blockchain Group announced it secured approximately €12.1 million through a convertible bond issuance reserved for Adam Back, CEO of Blockstream.

This post The Blockchain Group Secures €8.6 Million to Boost Bitcoin Strategy first appeared on Bitcoin Magazine and is written by Oscar Zarraga Perez.

-

@ cae03c48:2a7d6671

2025-05-21 20:00:50

Bitcoin Magazine

Building FUN! on Bitcoin: Parker Day and Casey Rodarmor Talk Collaboration and the Future of On-Chain Art and AuctionsParker Day and Casey Rodarmor’s FUN! Collection is an unprecedented synthesis of photographic maximalism and protocol-level innovation—a work that stands alone within the landscape of Bitcoin-native art. Saturated with Day’s bold color palette, surreal personas, and layered identity play, the collection is anchored by Rodarmor’s foundational role as the creator of the Ordinals protocol. Most notably, the series is inscribed directly under Inscription 0—the first inscription ever made using the Ordinals Protocol—marking it as an ontological outlier in the digital art canon. No other collection occupies this same foundational location on-chain, making FUN! a conceptual and technical landmark in Ordinals history.

Now expanded with new reflections from both collaborators, this interview explores the project’s deeper ideological dimensions—from the mechanics of trustless auctions to the ethics of artistic compensation, from pro wrestling and portraiture to capitalist generosity and the social roots of value. Together, Day and Rodarmor form a rare creative pairing: artist and dev, photographer and protocol architect, equal parts absurdity and rigor.

One of the collection’s most iconic works—featuring Rodarmor himself—is set to headline the Megalith.art auction, a Bitcoin-native sale structure that concludes on June 3rd and will be showcased at both Bitcoin 2025 in Las Vegas and its satellite event, Inscribing Vegas. The piece anchors a broader lineup that includes standout contributions from leading digital artists such as Post Wook, Coldie, Ryan Koopmans, FAR, Rupture, and Harto.

It’s less an interview than a glimpse into a high-voltage collaboration:

Parker, your photography is known for its bold color, eccentric characters, and fearless exploration of identity and persona. How did this collaboration with Casey come about, and what visual or cultural influences helped shape The FUN! Collection?

PARKER: Casey and I have known each other since high school. You could even say he was one of my first models—I shot his portrait for my sophomore year darkroom photography class. We kept in touch over the years, and in 2017 he encouraged me to turn my ICONS series into crypto art. I passed on that at the time, but in 2021 I did release an Ethereum NFT collection of ICONS. Right after that, Casey called me and said, “Yo! You need to go even bigger! Do 10k!” And I’m like, “You know these are all unretouched and shot on film, right?” But with his encouragement and funding, we figured out how to produce 1,000 unique portraits.

The visual and cultural influences behind FUN! are too numerous to name—just a mishmash of pop culture that’s been stewing in my brain since childhood.

The FUN! collection was released under a CC0 license, meaning anyone can reuse, remix, or recontextualize the work without restriction. In a project so rooted in persona, authorship, and performance, what led you to make that decision—and how do you think about authorship or artistic control in the context of open licensing on Bitcoin? What would you find interesting to see done with the collection beyond your original photography methodology? What kinds of reinterpretations or mutations of the collection would genuinely intrigue you?

PARKER: I love it. As an artist, once you create something and it leaves the studio, it’s out of your hands. The audience shapes the work in their own interpretations. You have no control over it. It seems silly to say “this is my IP, you can’t do anything with it.” We live in a world of memes, of reproduction ad infinitum. It seems anachronistic in today’s world to clutch copyright with an iron fist. And it’s perfectly in keeping with the ethos of Bitcoin to make the work CC0. In terms of value, the inscriptions are the scarce collectibles. Even more so than any editioned prints will ever be. Their inscriptions’ provenance is on chain, directly descended from inscription 0.

There’s nothing in particular that I’d like to see or not like to see done with FUN! I just hope people find meaning in it, and make meaning from it.

You two have an unusual creative relationship: artist and protocol dev, patron and co-conspirator. Casey, you basically invented a new medium to support Parker’s work. What does it mean to build something enduring together in a space that often prizes individualism?

CASEY: I love it. I mean—I really love it. Parker and I are super complementary. We each have our own strong wheelhouses, and we’re always engaging with each other’s work, but in this very chill, supportive way.

Like, when we’re shooting, I’ll tell her what I think looks cool or what might work well in the collection—but it’s never directive. It’s more like, “Hey, here’s some data. Do with it what you will.” And same goes for the technical stuff. We’ll talk about metadata, domains, the website layout—she gives me her thoughts, and it’s just… input. Take it or leave it.

We’re both so solid in our own lanes that it makes collaboration easy. There’s no weird insecurity. She’s the creative force behind the collection—I know that. I’m the technical backbone—and she knows that. That kind of clarity makes it fun.

And honestly, I’m just really proud of this partnership. We’ve been in each other’s lives in a positive way for so long—since high school. Parker’s given me Bitcoin haircuts. I was bugging her to do NFTs in 2017. Even when we’d go long stretches without talking, we always checked back in.

“Hey, how’s it going?”

“Saw you on Twitter.”

“Saw you on Instagram.”It’s just one of those great, long-running collaborations that’s rooted in mutual respect—and a shared willingness to go weird.

Casey, did you draw on any past modeling experience—or take notes from Raph? And what was it like working under Parker’s direction: more Kubrick or camp counselor?

CASEY: I think I was pretty self-directed for the shoot. I wasn’t drawing on past modeling experience exactly—more like theater kid energy. I’ve always loved professional wrestling. It’s incredibly cool… and also incredibly formulaic, so I get bored if I watch too much. But every couple of years, I check back in, see what the storylines are.

For this shoot, I knew exactly how I wanted to ham it up—like a professional wrestler. That wild, sweaty, insane energy. The spiked ball pressed against my face. All the weird faces. American pro wrestling is super operatic, honestly.

The character I was channeling? Mostly Ultimate Warrior. Parker really nailed the eyes—those classic, intense Ultimate Warrior eyes. He wore wild makeup and had that jacked-up look. Ric Flair was another influence—mainly for the hair. He had this long blond hair, and when it got bloody in the ring, it looked insane.

As for Parker—definitely more camp counselor than Kubrick. She sets the scene: everything ready, hair and makeup dialed, wardrobe laid out. We talked through the costumes a bit. She’ll give direction, a few hints here and there—but it’s really up to the model to bring it.

You can include that (Casey snaps his fingers.)

Yeah. You know? You know.

The FUN! collection features an interactive website where visitors can filter portraits by mood, prop, background color—even astrological sign. What inspired that kind of functionality?

PARKER: Before FUN!, I had been thinking about an exhibition that grouped photos based on emotional expression. Even though the personas may appear wildly different, the core humanity is the same. I’ve always tried to equate disparate identities by shooting people in the same way—with simple fabric backdrops that strip away time and place.

The FUN! website (fun.film), reflects this idea: difference in sameness, or sameness in difference. It’s a tool for play—but also a way to reflect on identity in a fragmented age.

Casey, you’ve described yourself as a capitalist—but you’ve also given away tools for free and pursued an almost obsessive elegance in your work. How do you reconcile market belief with this ethic of generosity? And what does that tension mean for the future of Ordinals?

CASEY: There’s absolutely no tension—and that’s because most people just don’t understand what capitalism is. Like, I can’t even begin to unpack what people think capitalism means.

Capitalism simply means the means of production are privately controlled. That’s it. That’s the whole definition. The alternatives? You’ve got two: either (1) violent chaos, or (2) the government owns and allocates all capital. That’s it. Those are your three options.

So when people say they’re “anti-capitalist,” what they usually mean is: “I want the government to control who gets what.” I’m not about that. I’m a staunch capitalist. I allocate my own means of production—my computers, my resources, my energy—how I see fit, not how the state tells me to.

And sometimes? That allocation includes giving things away. That’s not anti-capitalist. If the government confiscated my stuff and handed it out? Sure, that’s anti-capitalist. But me choosing to make something—sometimes selling it, sometimes not—is 100% aligned with the spirit of capitalism.

People need to get with the program.

You asked about the tension between generosity and profit in Ordinals? There _i

-

@ 000002de:c05780a7

2025-05-21 20:00:21

I enjoy Jonathan Pageau's perspectives from time to time. He is big on myth and symbolic signs in culture and history. I find this stuff fascinating as well. I watched this video last week, and based on the title, I was thinking... hmm, I wonder if it is a review of Return of the Strong Gods. It wasn't, but it really flows with the thesis of that book. You should read it if you haven't, and before you do, go check out @SimpleStacker's review of it.

Pageau starts the video by talking about the concept of "watching the clown." He uses Ye as the clown. Ye has been a leading indicator in the past when he publicly claimed he was a Christian and began making music and holding church services. Now he's going "off the rails" seemingly with his Hitler songs and art. Clearly, the stigma of Hitler will not last forever. It's hard for us to realize this. At least for someone of my age, but Pageau points out that eventually, the villains of history become less of a stand-in for Satan and more of a purely historical figure. He mentions Alexander the Great as a man who did incredibly evil things, but today we just read about him in school and don't really think about it too much. One day, that will be the way Hitler is viewed. Sure, evil, but the power of using him as the mythical Satan will wane.

The most interesting point I took away from this video, though, was that the post-war consensus was built on a dark secret. Now, it's not a secret to me, but at some point, it was. And this secret is a deep flaw in the current state of the West that keeps affecting us in negative ways. The secret is that in order to defeat Hitler and the Nazis, the West allied itself with the Soviets. Stalin. An incredibly evil man and an ideology that has led to the death and suffering of more humans than the Nazis. This is just a fact, but it's so dark that we don't talk about it.

For many years as I began to study Communism and the Soviet Union I began to question why on earth did the allies align themselves with Stalin. Obviously it was for stratigic reasons. I get it. But the fact that this topic is not really discussed in our culture has had a dark effect. Now, I'm not interested in figuring out if Stalin was more evil than Hitler or if Fascism is worse that Communism. I think this misses the point. The point is that today if soneone has Nazi symbols it is very likely not gonna go well for them but Communist symbols are usually just fine. We see the ideas of Socialism discussed openly without concern. Its popular even. Fascism on the other hand is always (until recently) masked at best.

Today we are seeing more and more people openly talk about this reality, and it is a signal that the WW2 consensus is breaking. As people age out and our collective memory fades, this lie will become more visible because the mythical view of Hitler will fade. This will allow people to be more objective about viewing the decisions of the past. I don't recall the book discussing this directly, but it is an interesting connection for sure.

I recommend watching The World War II Consensus is Breaking Down by Jonathan Pageau.

https://stacker.news/items/985962

-

@ 8bad92c3:ca714aa5

2025-05-21 19:01:59

Marty's Bent

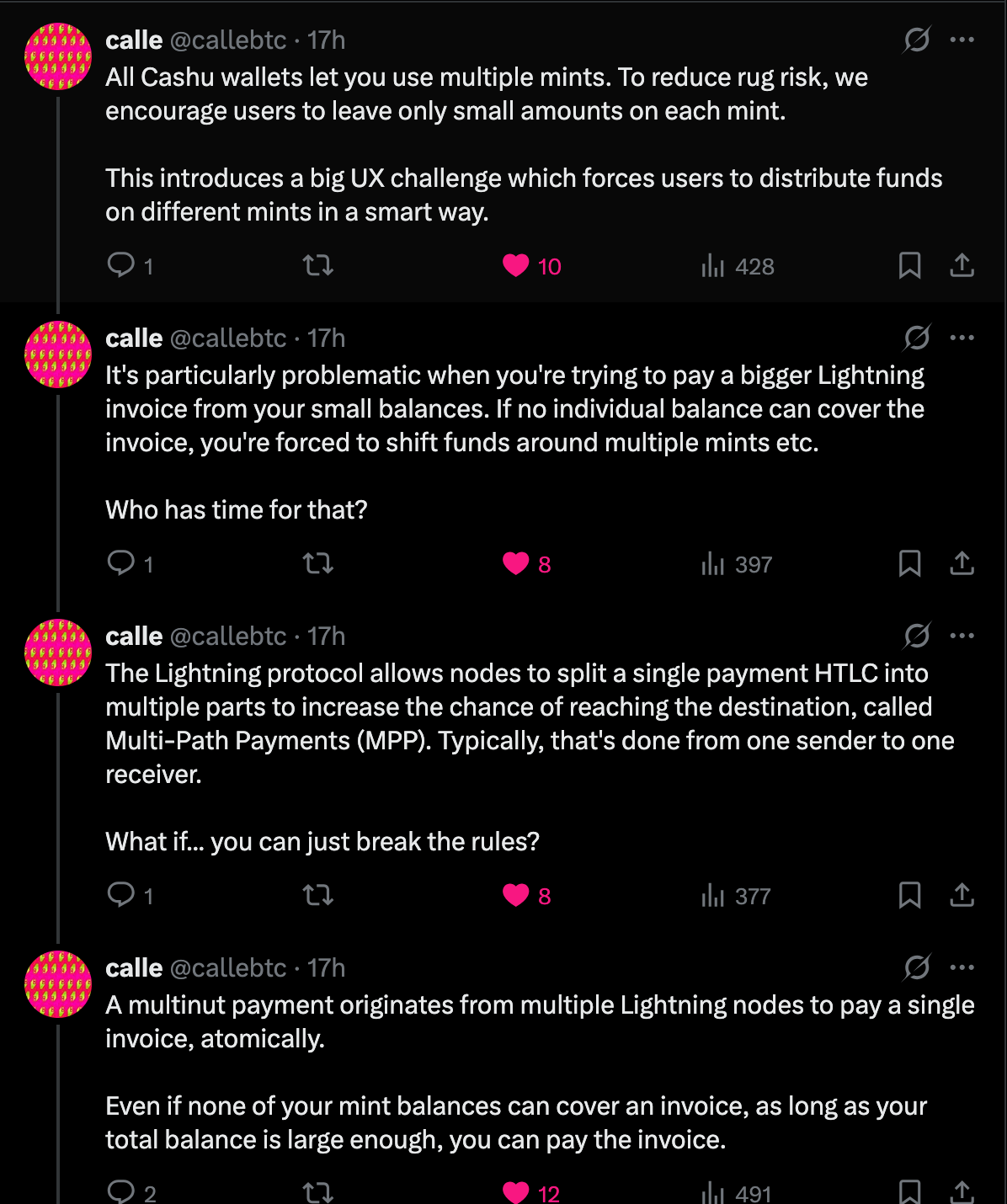

My god, this blows my mind. Paid a 100k sats invoice from two different Cashu mints at the same time. Each contributed 50k sats.

This is going to a major game-changer for @CashuBTC wallet UX.

Let me explain multinut payments. https://t.co/PvgTPvfvIv pic.twitter.com/d4cPVX7XKK

— calle (@callebtc) May 5, 2025

via calle

While many are currently wrapped up in press releases from public companies announcing that they've added to their Bitcoin treasuries, flame wars over OP_RETURN limits, or more general geopolitical developments cypherpunks are writing code. While the masses, many in Bitcoin included, are enthralled in day-to-day clickbait banter, there are serious builders building serious things at the moment. One of those builders is our friend calle, who - alongside other open source contributors - is building out the Cashu protocol, which enables individuals to leverage Chaumian ecash on top of bitcoin.

Earlier today, he demoed a pretty notable breakthrough for the Cashu protocol, a multinut payment, which enables users to pay a Lightning invoice by combining balances held in two separate Chaumian mints. For those of you who are unaware or need a refresher on Chaumian mints, they enable an individual to lock up a certain amount of bitcoin in a mint and receive a commensurate amount of ecash tokens in return. Chaumian mints leverage a blinded signature scheme to ensure that individual users have privacy while they're spending their ecash tokens.

Users lock up bitcoin in a mint, the mint issues tokens of different denominations to those users and after the user receives their tokens the mint has no idea which individual user is spending which ecash tokens within the mint. This increases the privacy of individual users on top of the privacy benefits. Spending with ecash comes with instant settlement, very low fees and is interoperable with other second layer solutions like the Lightning Network.

When users decide to engage with Chaumian mints, they are making a trade-off. They are trusting the individual mint operators not to steal their funds or debase the ecash tokens within their mints for the ability to transact privately, cheaply, and across multiple different interoperable protocols. While this is certainly a trade-off that no one should take lightly, I think it is important to understand that these Chaumian mint protocols like Cahu are permissionless, which means that anyone can leverage the open source code these protocols are built on to spin up their own mints, enter the competition for bitcoin banking services and serve end users.

Due to the very low barrier to entry that exists among these mint protocols like Cashu, I don't think it's crazy to say that competition can be a forcing function for mint operators to act in the best interest of their end users. I strongly believe that Chaumian mints are going to be a vital part of scaling bitcoin to billions of users over the coming decades. And this feature that calle demoed earlier today is going to be a very crucial component of that scaling process. Enabling individual users to distribute risk across many mints is going to be crucial to create the competitive landscape necessary for an incentive framework from which mint operators are pressured by the market to provide reliable and valuable services. Unlocking the ability to combine balances from multiple mints to pay a single invoice is an incredible step in that direction.

Imagine having to pay a landscaper for doing work and you have money on Cash App, Venmo, and PayPal, all of which you don't fully trust. However, you keep a small balance on each of them just in case you need to spend between friends or with certain vendors. The landscaping bill is a bit heftier than it typically is, so instead of sending funds from Cash App, Venmo, and PayPal to your bank account to then pay the landscaper instead, you combine part of the balance from each application to pay the singular invoice the landscaper has provided you. That is essentially what has just been launched on the Cashu protocol.

This is just the tip of the iceberg. I'm extremely excited to see the continued development of all Chaumian mint protocols and the use cases they enable. The Achilles heel of these protocols up to this point is the fact that users are incentivized to concentrate risk with individual mint operators to solve payment UX problems. Multinut payments alleviate that risk and intensifies the forcing function of competitive market dynamics that should lead to better end products for users of these protocols.

I've said it many times but I'll say it again. There are many discussions being had about how to scale bitcoin at the protocol layer. I think it is unwise to depend on changes to the protocol layer to scale bitcoin. We have many tools at our fingertips to scale bitcoin to billions today - that come with certain tradeoffs - that have not been tested. Multinut payments a great example of ways to scale bitcoin with the tools that are at our fingertips right now.

Most are completely missing it, but the cypherpunk future is being built out right before our eyes. Number go up and semantic dick measuring contests can certainly draw a lot of attention, but I implore you to rise above the noise and follow projects like this, which are actually solving massive user experience pain points in real time with things that can be used today.

Pensions Facing a Second "Lost Decade" Without Bitcoin Adoption

Dom Bei, a firefighter running for CalPERS' Board of Trustees, delivered a compelling warning during our recent conversation. He pointed out that CalPERS' outgoing Chief Investment Officer described missing the private equity boom as their "lost decade." Bei argues that pension funds nationwide are setting themselves up for another missed opportunity by ignoring Bitcoin, leaving them perpetually underfunded while seeking increasingly risky traditional investments.

"Are you going to have similar commentary from pensions around the country in 2035 saying, 'Hey, we're going to get into Bitcoin now. We had a lost decade where it was just staring us right in the face and we didn't really need to do much, but learn about it. And we missed the boat.'" - Dom Bei

I've long maintained that institutional adoption of Bitcoin is inevitable, but timing matters tremendously for returns. With CalPERS sitting at just 75% funded and facing high CIO turnover, Bei's approach of education and incremental adoption offers a practical path forward. The volatility fears that keep pensions away from Bitcoin can only be addressed through proper education—something severely lacking in these massive financial institutions managing trillions in retirement funds.